Most fintech pitch decks fail for a simple reason: they try to explain the business before they’ve structured the story correctly.

This guide focuses on the practical mechanics of building a fintech pitch deck—how it’s structured, what each slide is responsible for, and how information is typically organized at the execution level. It is written for founders who already understand what they are building and now need to translate that into a deck that functions properly in review environments.

What follows is not a theory of fundraising, nor a discussion of capital strategy. It is a hands-on guide to assembling a fintech pitch deck that does its job.

Decision logic, sector rules, and capital assessment frameworks are defined upstream—particularly in the fintech capital evaluation context—which outlines how fintech businesses are reviewed at a strategic level.

What a Fintech Pitch Deck Is (Execution Definition)

At the execution level, a fintech pitch deck is a structured review artifact.

It is not a business plan, a technical specification, or a full diligence package. Instead, it functions as a compressed narrative container—a document designed to summarize a fintech company’s problem, solution, market positioning, and operating model in a format that can be quickly reviewed, shared internally, and referenced across multiple stages of discussion.

Practically speaking, a fintech pitch deck serves three execution purposes:

- Orientation – It gives reviewers enough context to understand what the company does, who it serves, and how it operates, without requiring external explanation.

- Structure – It organizes information in a predictable sequence so key elements (market, model, traction, financials) can be located and assessed efficiently.

- Reference – It becomes a reusable document that supports follow-up conversations, internal circulation, and comparison with other opportunities.

From an execution standpoint, the quality of a fintech pitch deck is determined less by how persuasive it sounds and more by how clearly it presents information, how well it respects expected slide roles, and how consistently it avoids common structural errors. A well-built deck reduces friction in review by making the company easier to understand—not by attempting to argue the decision itself.

Standard Fintech Pitch Deck Length & Format

Standard Fintech Pitch Deck Length & Format

From an execution standpoint, a fintech pitch deck is expected to be concise, scannable, and structurally predictable. Length and format choices are not about persuasion; they determine whether the deck can be reviewed efficiently and referenced without friction.

Typical Slide Count

For most fintech startups, the core deck typically falls within 10 to 14 slides. This range is not arbitrary—it reflects how much information can be reviewed in a single pass without losing structural clarity.

- 10–12 slides is common for early-stage fintech startups, where the goal is to establish context, model clarity, and baseline credibility.

- 12–14 slides may be used when additional explanation is required, such as more complex revenue mechanics, regulatory positioning, or multi-sided markets.

Exceeding this range often introduces redundancy rather than clarity, especially when slides begin to repeat the same idea in different forms.

Short Deck vs. Extended Deck

Execution-wise, fintech teams usually maintain two versions of their pitch deck:

- A core deck (the main 10–14 slides) used for initial review and circulation.

- An extended version or appendix that includes deeper detail—expanded financials, regulatory notes, technical architecture, or supporting data.

The core deck should stand on its own. Any extended material is best treated as optional reference, not required reading.

File Format and Delivery

The standard format for fintech pitch decks is PDF. This ensures layout stability, consistent viewing across devices, and easy internal sharing. Live presentation formats are sometimes used for meetings, but the underlying deck is still expected to function as a standalone document when circulated without narration.

Key execution considerations:

- Fixed aspect ratio (typically 16:9)

- Clear visual hierarchy for quick scanning

- Text density controlled to avoid “document-style” slides

Appendices and Supporting Slides

Appendix slides are acceptable, but they should be clearly separated from the main narrative. Common appendix content includes:

- Detailed financial models or assumptions

- Expanded regulatory context

- Technical architecture diagrams

- Market research tables

At the execution level, appendices exist to support follow-up, not to compensate for unclear core slides.

Consistency Over Volume

More slides do not equal more information. Well-structured fintech pitch decks prioritize consistency, sequencing, and restraint over volume. A shorter deck with clearly defined slide roles is typically easier to review than a longer deck that attempts to anticipate every possible question upfront.

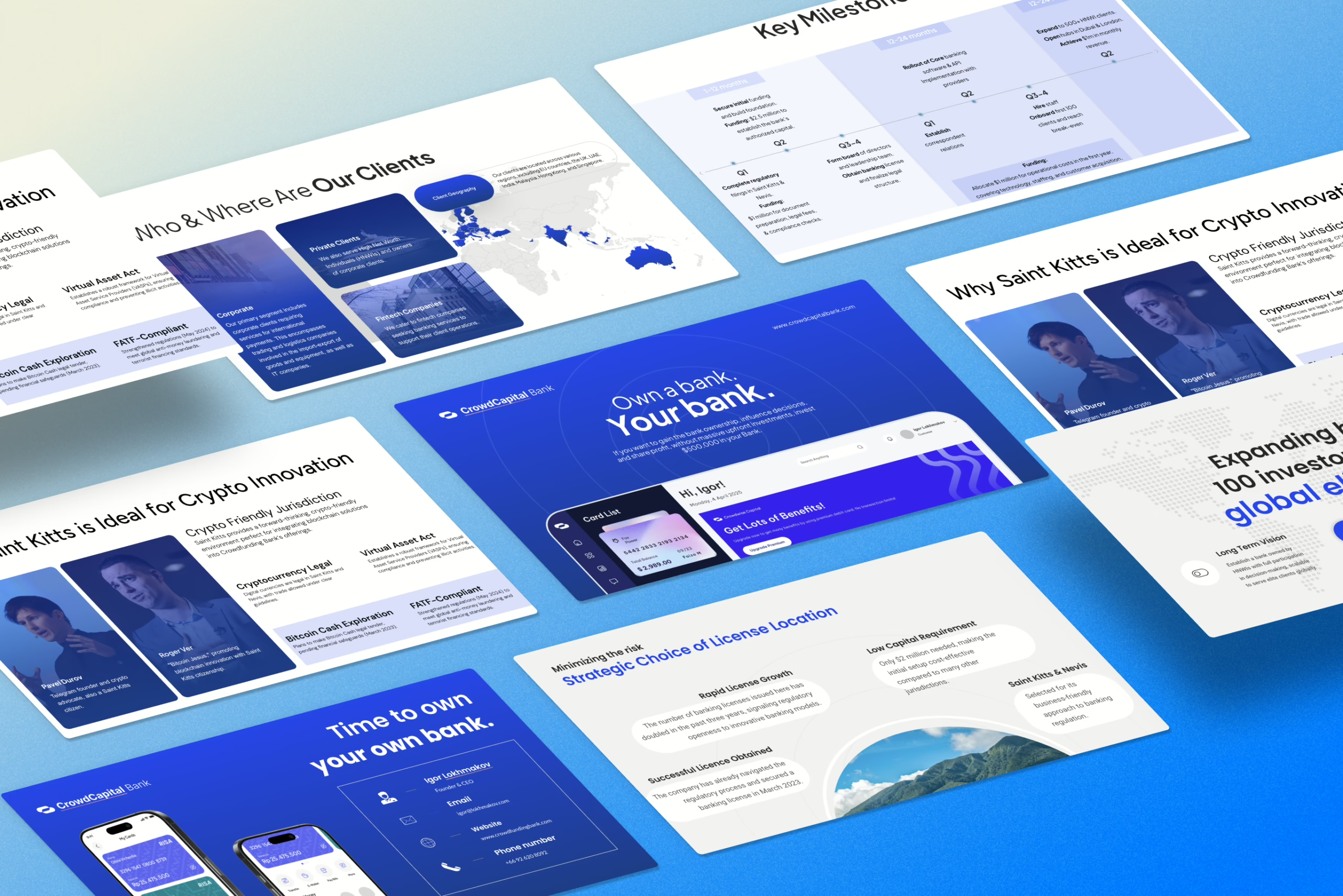

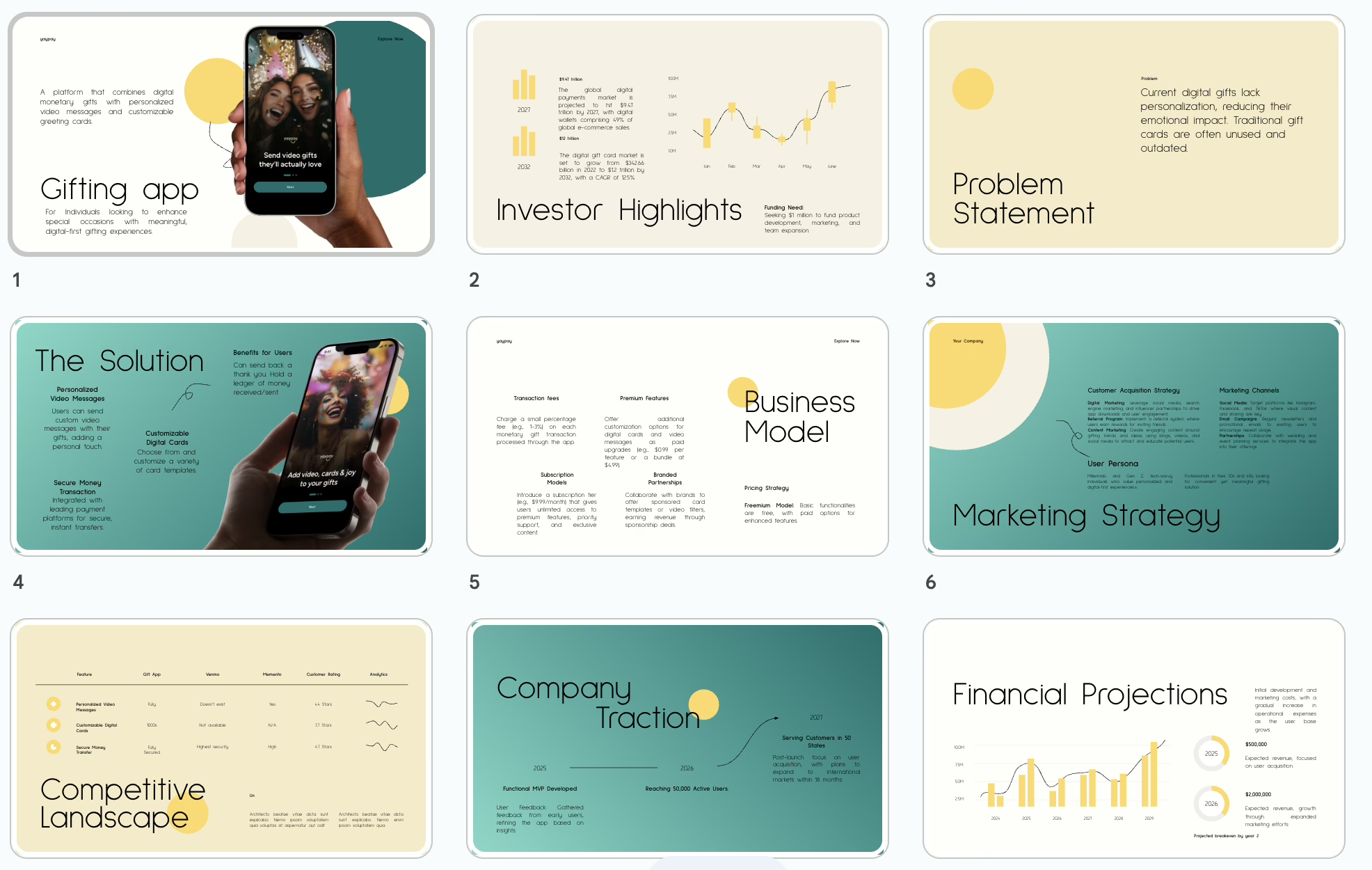

The 10-Slide Fintech Pitch Deck Structure (Execution Template)

1. Cover / Context Slide

Purpose: Establish immediate context.

This slide typically includes the company name, a one-line descriptor, and a clear indication of what the business does. At the execution level, its job is orientation—not explanation. Reviewers should understand the category and scope of the business within seconds.

Common execution issues:

- Vague taglines that require interpretation

- Overdesigned visuals that obscure basic context

2. Problem Slide

Purpose: Define the operational or market problem being addressed.

This slide frames the problem in concrete, observable terms. In fintech, this often involves inefficiencies in payments, access, compliance, cost, or infrastructure. The slide should describe the problem clearly without attempting to prove its importance.

Common execution issues:

- Multiple unrelated problems on one slide

- Abstract language instead of real-world conditions

3. Solution / Product Slide

Purpose: Show how the product addresses the stated problem.

This slide introduces the product or service at a functional level. It should explain what the product does and how it fits into the workflow, not how advanced or differentiated it is.

Common execution issues:

- Turning the slide into a feature list

- Using screenshots without context

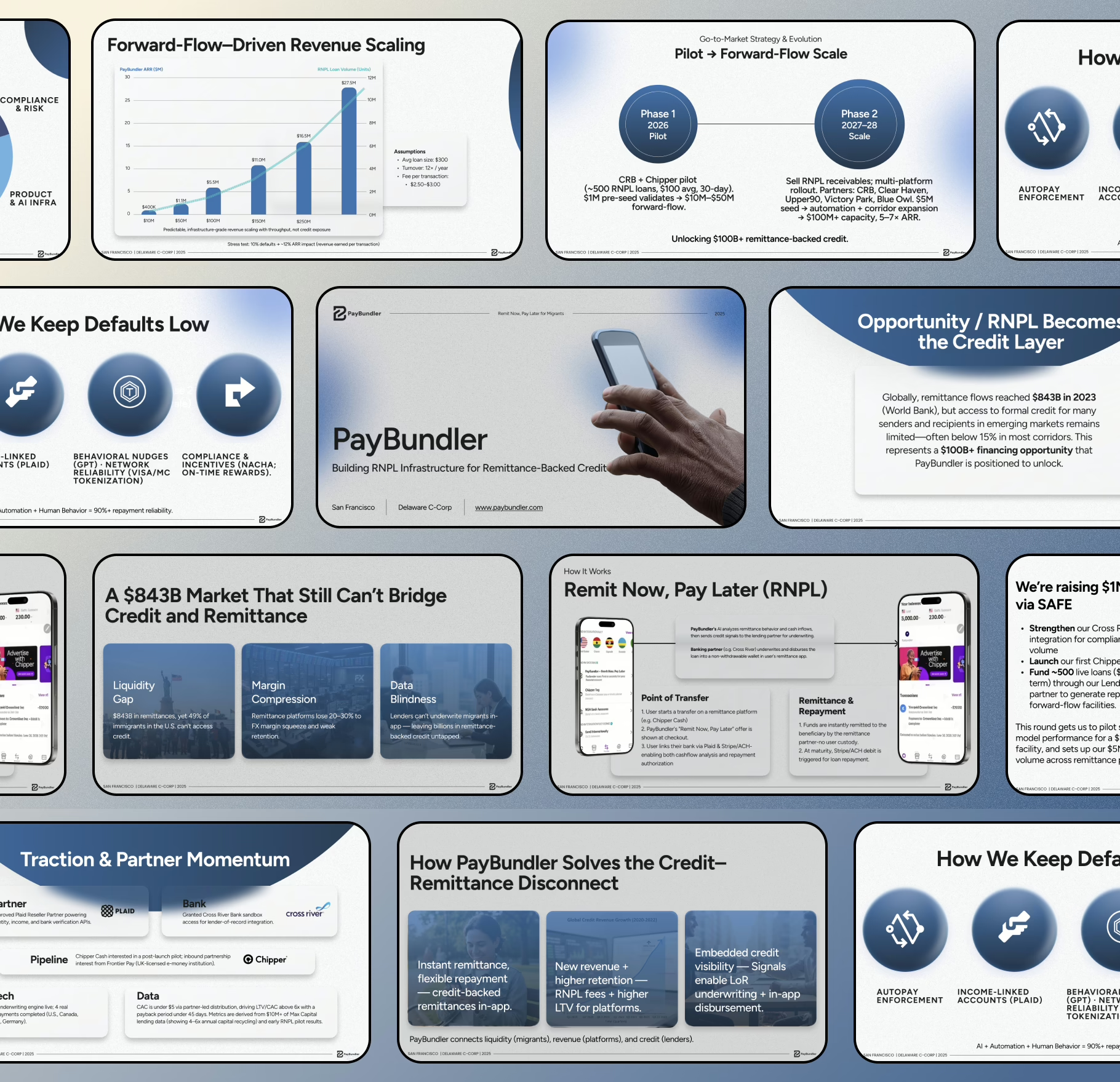

4. Market Opportunity (TAM / SAM / SOM)

Purpose: Present market sizing in a structured, legible format.

This slide shows how the market is segmented and quantified. The emphasis is on clarity of scope and internal consistency between numbers, not on maximizing perceived size.

Common execution issues:

- Inflated totals without explanation

- Numbers that don’t align with the product scope

5. Business Model

Purpose: Explain how the company generates revenue.

This slide outlines pricing logic, revenue streams, and unit-level mechanics. In fintech decks, clarity matters more than completeness—reviewers should be able to trace how usage turns into revenue.

Common execution issues:

- Revenue described without linkage to product usage

- Multiple models presented without prioritization

6. Traction & Signals

Purpose: Show evidence of progress or validation.

Traction slides summarize relevant indicators such as users, revenue, pilots, partnerships, or operational milestones. At the execution level, this slide is about signal selection, not storytelling.

Common execution issues:

- Mixing vanity metrics with operational metrics

- Presenting raw numbers without timeframe

7. Technology / Infrastructure

Purpose: Explain how the product is built at a high level.

This slide provides a simplified view of the technical foundation—APIs, platforms, integrations, or infrastructure dependencies. It should remain readable to non-technical reviewers while still being precise.

Common execution issues:

- Overly detailed architecture diagrams

- Technical jargon without explanation

8. Regulatory / Risk Awareness

Purpose: Acknowledge relevant constraints and safeguards.

This slide demonstrates awareness of regulatory, compliance, or operational constraints relevant to the business. It should communicate preparedness without turning into a legal explanation.

Common execution issues:

- Overloading the slide with regulatory detail

- Avoiding the topic entirely

9. Financials & Projections

Purpose: Summarize financial direction and assumptions.

This slide typically includes high-level projections, revenue growth, cost structure, and key assumptions. The focus is on internal coherence and readability, not precision modeling.

Common execution issues:

- Dense tables that require narration

- Projections disconnected from the business model slide

10. Team & Execution Capability

Purpose: Show who is responsible for execution.

This slide introduces the core team and their relevant experience. Execution-wise, it should connect people to functions, not list credentials exhaustively.

Common execution issues:

- Long bios with no relevance to the business

- Missing operational roles

Fintech-Specific Slides Founders Often Get Wrong

Fintech decks don’t usually break because founders “forgot a slide.” They break because certain slides carry more operational load in fintech than founders expect—and the execution gets messy: too much detail, wrong format, unclear boundaries, or mismatched metrics.

Below are the slides that most often fail at the mechanics level (structure, specificity, and how information is presented), even when the business itself is solid.

1) Business Model Slide (pricing ≠ model)

Common execution failure: describing pricing without explaining how revenue is generated per workflow.

A fintech business model slide should map who pays, when they pay, what triggers payment, and how usage converts to revenue. If the slide can’t be read like a simple flow (“X happens → Y fee → Z margin”), it’s underbuilt.

Fix (mechanical):

- Use a 3–5 step flow (user action → transaction → fee → cost → margin).

- Show 1–2 primary revenue streams, not seven “options.”

- Keep the math readable: one unit example beats a paragraph.

2) Traction Slide (numbers without a clock)

Common execution failure: metrics without a timeframe, baseline, or definition.

Fintech traction slides often list impressive numbers that can’t be interpreted because there’s no period (monthly vs cumulative), no denominator (per customer? per account?), or no “what counts.”

Fix (mechanical):

- Put time in the headline (“Last 6 months,” “Q3–Q4 2025”).

- Add definitions in tiny text (what is an “active user,” what counts as “TPV”).

- Prefer 3–6 metrics max, all consistent in timeframe.

3) Financial Projections Slide (tables that require narration)

Common execution failure: dumping a spreadsheet into a slide.

The deck doesn’t need a model; it needs a readable summary that matches your business model slide and traction slide.

Fix (mechanical):

- Show 3-year top-line + 2–3 drivers (not a 20-line P&L).

- Make sure drivers match slide 5 (pricing/revenue logic).

- If you must include a table, keep it under 8 rows and under 5 columns.

4) Regulatory / Risk Awareness Slide (either fear-mongering or denial)

Common execution failure: founders either over-lawyer the slide or avoid it entirely.

Execution-wise, the slide should show awareness + containment, not a regulatory essay.

Fix (mechanical):

- Use a simple 3-column layout: “Exposure / Control / Current Status.”

- Keep it to 4–6 bullets total.

- Avoid claiming approvals you don’t have; state status plainly.

5) Technology / Infrastructure Slide (architecture porn)

Common execution failure: complex diagrams that confuse more than they clarify.

This slide should make it easy to understand what the product integrates with, what you own, and what depends on partners.

Fix (mechanical):

- Use a layered diagram: “User layer / Product layer / Integrations / Data.”

- Label with human words, not internal system names.

- One diagram + one sentence is usually enough.

6) Market Sizing Slide (big numbers, weak scope)

Common execution failure: market sizing that doesn’t match the actual product scope.

Execution-wise, your TAM/SAM/SOM must be legible and scoped, not theatrical.

Fix (mechanical):

- Make your segments match your ICP (not the entire global economy).

- Show method in one line (top-down or bottoms-up).

- Keep numbers aligned (no sudden leaps between layers).

Common Execution Mistakes in Fintech Pitch Decks

This is the part founders hate because it’s painfully fixable. These aren’t “business problems.” These are deck construction problems—and they create confusion, rework, and misreads.

1) Slide roles are unclear (everything tries to do everything)

A common fintech deck issue is that slides don’t have boundaries. The “Solution” slide becomes a product demo, a strategy memo, and a feature list. The result is bloated, unfocused, and hard to scan.

Execution fix: one slide = one job. If a slide needs narration to be understood, it’s doing too much.

2) Sequencing is off (reviewers can’t build the mental model)

Even strong content breaks when the order is wrong. If the deck jumps into traction before explaining the model, or dives into tech before establishing the problem, the reader can’t assemble a clean narrative.

Execution fix: keep the structure stable (problem → solution → market → model → traction → risk → financials).

3) Metric chaos (definitions drift from slide to slide)

Fintech decks often swap metric definitions mid-deck: “customers” means accounts on one slide and paying businesses on another; “revenue” means GMV somewhere else. That’s not a debate. That’s a drafting error.

Execution fix: define metrics once, keep them consistent, and reuse the same timeframe across slides.

4) Visual density is too high (slides become documents)

Fintech founders love detail. Slides don’t. Walls of text and micro-tables make the deck unreadable on first pass.

Execution fix: reduce slide content to headline + 3–5 bullets + one visual. Put the rest in appendix.

5) Claims are written like marketing copy

“Revolutionary,” “best-in-class,” “unmatched,” “game-changing.” These words don’t clarify anything and they inflate slide weight.

Execution fix: replace adjectives with specifics (what it does, for whom, how it works, what changed).

6) Too many “optional” business models

Many fintech decks list multiple business models as if they’re menu items. Execution-wise, this creates ambiguity: the reader can’t tell what you’re actually doing now.

Execution fix: present one primary model. If there’s a second, frame it as “later” with clear sequencing.

7) Risk slide is either missing or unreadable

Skipping risk entirely makes the deck feel naive. Over-explaining risk makes it feel fragile. Execution-wise, both are avoidable.

Execution fix: concise risk-awareness format: “Exposure / Control / Status” (4–6 bullets total).