When an investor says “no,” it rarely means your startup is worthless. It usually means: “given my fund, my thesis, my portfolio, and the risks I’m paid to absorb, I can’t justify an investment right now.” That distinction matters, because founders hear a moral judgment where the investor is making a portfolio decision.

A rejection also reflects the environment: investors are scanning for clarity under time pressure, comparing you against alternatives, and protecting reserves for companies they already invested in. That “already invested” dynamic quietly shapes many no’s — especially in tighter cycles when funds become conservative by default. This pattern is visible in how a fundraising pipeline behaves over time in the fundraising process.

Purpose of the article:

Most founders treat “no” as a dead end. The more useful interpretation is that “no” is a categorization event: the investor is labeling the dominant risk they see (market, team, product, execution, terms, timing), then passing on investing because that risk feels unpriced or uncontained.

This article is built to do three things:

- Reduce ambiguity. A startup can survive a “no.” It can’t survive not knowing what the “no” actually refers to.

- Separate fixable from structural. Some objections are addressable (missing role, unclear GTM, weak metric). Others are structural (their fund stage, sector focus, reserves, portfolio exposure).

- Make the next pitch structurally coherent. Not louder. Not “more persuasive.” Just more internally consistent: market → business model → traction → valuation → narrative.

This is also why investors ask for the same core slides again and again: the structure is a stress test, not a tradition. The way this is typically expressed inside a deck is mapped in what an investor pitch deck is.

Primary Reasons Investors Say No To Your Startup

Below are the dominant buckets that drive most rejections across angel investors, syndicates, and venture capitalists — from pre-seed through growth. (Different stages change the weighting, but the buckets stay boringly consistent.)

Market risk (small market, unclear market, poor timing)

Market risk shows up when the investor can’t underwrite the size, urgency, or buying behavior of the market. “Big” doesn’t mean a large number in a slide; it means budget exists, the buyer knows they have a problem, and adoption isn’t a decade-long science project.

This is why vague market sizing creates friction: if TAM is inflated or undefined, the investor can’t tell whether the outcome is “category-scale” or “nice lifestyle business.” The difference is often expressed through the sizing logic behind TAM/SAM/SOM, which is structurally mapped in TAM, SAM, and SOM in a pitch deck.

Team concerns (missing roles, shallow domain depth, execution mismatch)

Team concerns aren’t only “inexperience.” They’re usually about fit for the next 18 months: who sells, who ships, who closes partnerships, who survives inevitable setbacks without drifting.

Investors also look for role coverage: if you’re B2B and the team is all product, the sales motion becomes speculative; if you’re deep tech and the team is all business, the roadmap becomes speculative. In other words, the investor isn’t rejecting your résumé — they’re rejecting the probability distribution of execution.

This shows up in how different investors emphasize different proof points, which is why one deck format rarely fits all without structural adjustment (see tailoring a pitch deck for different investors).

Product risk (immature technology, weak differentiation, unclear product-market fit)

Product risk appears when the investor can’t see what makes the product meaningfully distinct — or can’t see why the market would adopt it now. “We’re better” doesn’t hold unless it’s backed by something that creates persistence: distribution leverage, integration lock-in, switching costs, proprietary data loops, or a wedge that competitors can’t casually copy.

A common failure mode is “feature soup”: lots of capabilities, no crisp “this is the job we do better than anyone else.” When that happens, the investor’s brain does what brains do under evaluation pressure: it collapses the story into “another one.”

This is often where the narrative breaks between “what it is” and “why it matters,” which is why the product’s positioning tends to be structurally expressed through a clear solution block (see the solution slide).

Signals Behind a “No”

Direct no vs. soft no (wording to watch)

A direct no is clean: “Not a fit,” “Too early,” “We’re not investing in this.” A soft no is socially polite but structurally identical: “Keep me posted,” “Let’s reconnect in a few months,” “Interesting — send more info.” Soft no language often reflects an investor trying to exit the conversation without conflict, not a request for a deeper relationship.

This dynamic reflects how human communication works in evaluation settings: vague language reduces social friction, but it increases founder confusion. Patterns like this show up in pitch communication behaviors, including how teams compress meaning into single lines (see one-sentence elevator pitch).

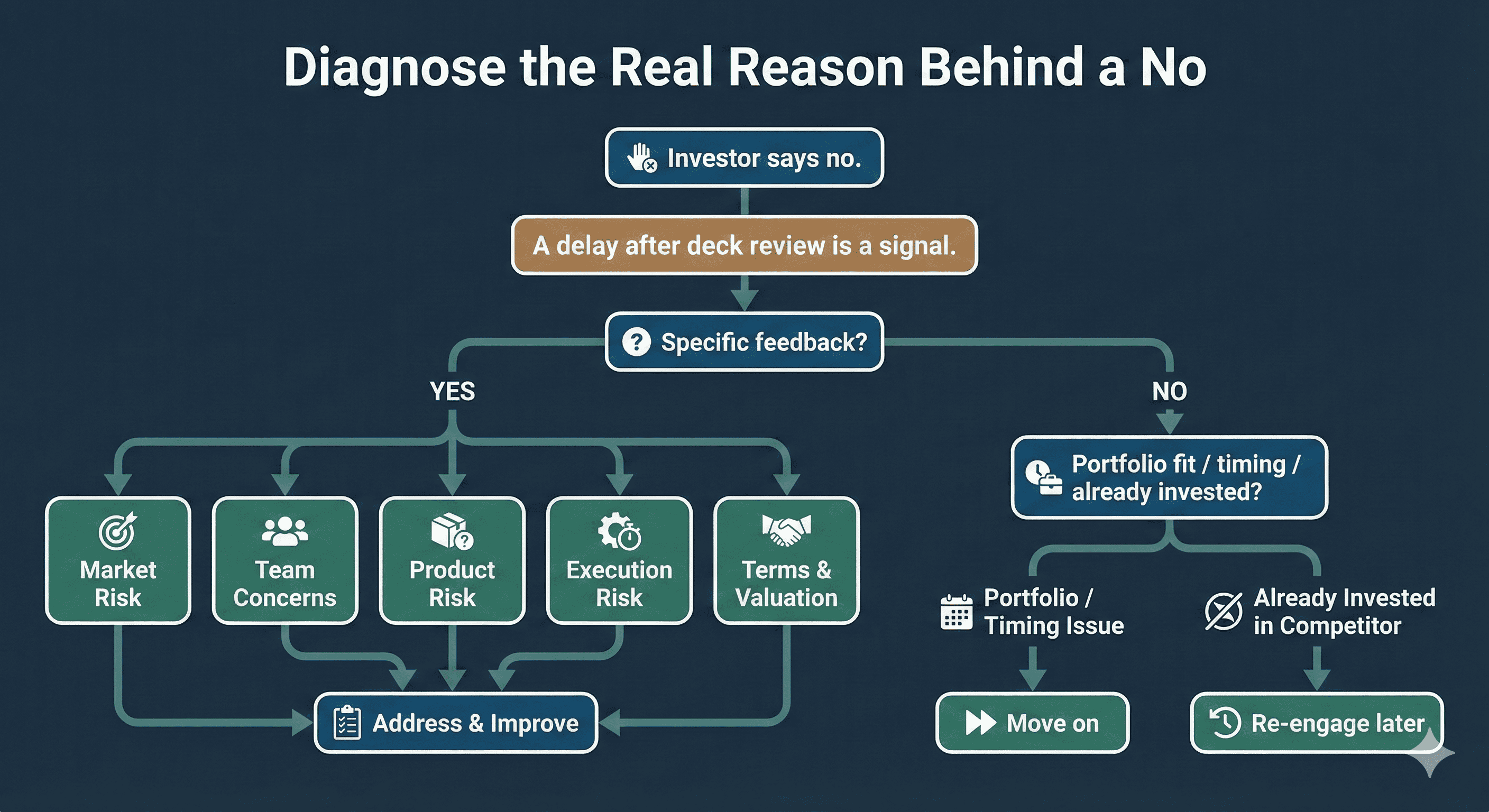

Timing and delays as indicators

Delays are a signal, not a mystery. If the investor goes from fast replies to slow replies after seeing the deck, that usually means the deck created a dominant objection they don’t want to debate. If delays happen before the deck is sent, it’s often just bandwidth.

Also: “timing” is sometimes real (fund constraints, portfolio exposure), and sometimes a polite wrapper around “I don’t see the shape of this yet.”

This pattern aligns with how information gets filtered when attention is scarce — investors default to simplification. You can see this compression behavior in the broader principle behind the art of simplification.

Request for more data vs. fundamental objection

Some “send more” requests are genuine: they want clarity on ARR, churn, pipeline, or cohort behavior. Others are a way to postpone an uncomfortable no.

A decent heuristic: if the investor asks for specific data tied to a decision (“what’s your payback period,” “what’s the sales cycle,” “what’s retention by cohort”), that reflects an evaluation in progress. If they ask for generic “more info,” it often reflects uncertainty that they don’t want to name.

The difference is typically visible in whether they’re probing traction and growth mechanics (see traction and growth in your pitch deck).

How to Diagnose the Real Reason

Ask clarifying questions politely

Diagnosis isn’t interrogation. The goal is to map the investor’s objection to a category without turning the conversation into a debate. Investors usually respond better to “I’m trying to understand which risk dominated your decision” than “why did you reject us?”

You’re not asking them to “change their mind.” You’re asking them to label the risk, so you don’t waste time fixing the wrong thing.

This is also why the same deck can get opposite reactions: two investors may be optimizing for different portfolio needs (“already invested,” reserve strategy, stage fit), not disagreeing about your company’s worth.

Request specific feedback and examples

General feedback is cheap. Specific feedback is expensive — and therefore more truthful. Examples force clarity: “Was it the TAM assumption, the GTM motion, the retention story, or the valuation?”

When the investor gives a concrete example, you can tell whether this is a “we don’t invest in this” no, or a “we don’t understand this yet” no. Even one line of specificity can save you weeks of guessing.

The structural place where this usually manifests is in the core narrative skeleton of a deck (see how to create a pitch deck).

Map objections to categories (team, market, product, terms)

Once you can name the category, you can stop spiraling. “Market” is not “team.” “Terms” is not “product.” Most founders lose time because they try to fix everything at once, which usually results in fixing nothing.

This isn’t about being defensive; it’s about making sure your next iteration expresses the right evidence in the right place — market sizing evidence belongs in market sizing, traction belongs in traction, and so on. (Investors love coherence. Humans love coherence.)

A simple example of category mapping: if the pushback is “I don’t see how you acquire customers efficiently,” that’s a GTM/execution objection, which tends to be structurally expressed through a clear go-to-market slide.

Follow-up strategy and timing

Follow-up isn’t persistence theater. It’s a test of whether something has changed in the risk picture. If nothing changed, following up is just asking for the same no twice.

If something did change (new ARR, pilot results, major hire, regulatory milestone), follow-up becomes rational because the investor’s prior objection may no longer dominate.

This is why update cadence matters — not too chatty, not too silent. The “right” cadence is the one where each update is a real signal, not noise. That’s also why founders often keep a one-page version around: it supports clean updates without overloading attention (see one-pager pitch deck).

Strategies to Address Common Objections

You don’t overcome investor objections by arguing. You overcome them by changing the evidence they’re using to price risk.

TAM Market objections: tighten the narrative, not just the numbers

When investors say “too small,” “too early,” or “unclear market,” they’re usually disputing economic inevitability, not math.

Fix it by:

- Replacing top-down TAM with bottom-up buyer-budget logic

- Naming the buyer, purchase trigger, and budget line item

- Showing customer validation (paid pilots, LOIs, conversion rates)

If your sizing is vague, investors can’t underwrite the upside. That’s why a strong TAM/SAM/SOM breakdown is one of the fastest ways to turn “unclear” into “credible.”

Team objections: prove execution capacity, not just talent

Team concerns are rarely about intelligence. They’re about whether the team is built to survive the next 18 months without drifting.

Fix it by:

- Patching missing roles (sales, engineering depth, regulatory, partnerships)

- Adding domain advisors who reduce execution uncertainty

- Showing complementary experience tied to the current stage

Different funds overweight different risks, which is why tailoring your pitch deck to the investor often changes outcomes without changing the company.

Product objections: eliminate feature soup and create wedges

When investors say “we’ve seen this,” it usually means your differentiation collapses under pressure.

Fix it by:

- Defining one dominant job-to-be-done

- Proving outcome superiority (not feature lists)

- Converting pilots into measurable case studies

This is why a crisp solution slide matters more than long explanations — it forces one coherent story.

Financial objections: replace forecasts with proof mechanics

If the investor rejects the model, they’re not offended by numbers — they don’t believe the business physics.

Fix it by:

- Showing unit economics that match your GTM

- Adding sensitivity analysis (CAC 2×, churn worse, sales cycles longer)

- Turning projections into proof milestones

The easiest way to make this believable is to anchor the story in evidence-heavy traction and growth framing.

Valuation objections: reframe risk instead of defending price

If the investor likes the company but rejects the valuation, they’re saying your certainty exceeds your evidence.

Fix it by:

- Using a SAFE/convertible structure when appropriate

- Offering milestone-linked tranches

- Cleaning cap table issues before bigger money

But don’t confuse “price” with “risk.” Lower valuation won’t fix a market or execution objection.

Competition objections: show leverage, not bravery

Incumbents aren’t the killer. No wedge is.

Fix it by:

- Defining your entry wedge

- Proving distribution advantage

- Showing switching costs or lock-in

Most competition objections disappear once your go-to-market strategy stops sounding like hope and starts sounding like a mechanism.

Regulatory objections: replace uncertainty with process

In regulated industries, “we’ll figure it out” translates to unpriced downside.

Fix it by:

- Mapping compliance pathways + timeline + ownership

- Cleaning IP ownership and assignments

- Documenting legal diligence where needed

When to Move On

Chasing reluctant investors is emotional labor disguised as optimism.

Signals the objection is structural

- “Outside our mandate”

- “Not our stage”

- “Not our sector”

- Persistent vagueness or repeated delays after you send data

Those aren’t business critiques — they’re portfolio constraints.

The cost of chasing the wrong investor

Every week spent trying to revive a dead “maybe” is a week not spent:

- improving traction

- building pipeline

- closing customers

- pitching better-fit funds

Fundraising isn’t persuasion. It’s alignment discovery.

Maintain optionality without becoming noise

Send updates only when risk materially changes (revenue, pilots, key hires, approvals). Keep it short. If you need a format that makes this easy, use a one-pager pitch deck as your recurring update asset.

Examples & Case Studies

Case 1: “The TAM SAM SOM is too small”

No: “This feels niche.”

Real issue: Market is unclear, not small.

Fix: Bottom-up TAM from buyer budgets + pilots + LOIs.

Result: Risk shifts from “uncertain market” to “execution opportunity.”

Case 2: “Come back when you have traction”

No: “Come back later.”

Real issue: Execution confidence gap.

Fix: Add key hire/advisor, clarify responsibilities, show pipeline stages.

Result: Risk shifts from “team doubt” to “speed of progress.”

Case 3: “We’ve seen this before”

No: “This isn’t differentiated.”

Real issue: No wedge; feature soup.

Fix: Narrow to one painful job + one advantaged channel + measurable outcome.

Result: You stop being “another tool” and become “the entrant.”

Investor Communication Best Practices

How to present pivots without losing trust

A pivot isn’t a confession. It’s a decision. Frame it as:

- what changed

- what you learned

- what you decided

- what evidence confirms it

Updates: signal-dense, not chatty

A good update has:

- one traction metric

- one product milestone

- one commercial milestone

- one optional ask

If it reads like a diary, it’s ignored like a diary.

Turn feedback into action items

Treat feedback like risk classification:

- market

- team

- product

- execution

- terms

Map the objection → adjust evidence → re-test.

This works best when your deck is structurally clean, which is why the baseline how to create a pitch deck guidance matters more than “storytelling tips.”

FAQ

1) Why do investors say no to a startup even when the idea looks good?

Most investors say no because they don’t see a risk-adjusted reason to say yes yet. The investor may believe the product is interesting, but they need to believe the company and investor fit is real: the market is large enough, the business model can scale, and there’s money to make without the story crashed and burned at the first bump. Investors are looking for proof that a first-time founder’s plan works under pressure — not just that it sounds smart in a pitch.

2) What are the top reasons why investors say no at pre-seed and early stage?

At pre-seed and early-stage, the most common reasons why investors say no are: unclear GTM, weak early validation (no credible prototype proof), messy logic on who buys and why now, and a shaky path to raising capital efficiently without immediate dilute pain. Early-stage VCs and angel investors also watch for founder track record, CEO clarity, and whether the deal can avoid an early exit trap or a cap table that scares future rounds.

3) What do VCs need to see before they invest in companies with low ARR?

Many VCs will invest before meaningful ARR, but investors need clear leading indicators: buyer urgency, repeatable sales motion, early retention/expansion signals, and a credible pricing model tied to acquisition cost. If an investor doesn’t see how your GTM turns into predictable revenue, they assume it becomes expensive fund raising with weak leverage. In plain terms: they want evidence the engine works, not just that the dashboard looks nice.

4) How do angel investors and syndicates decide whether to invest?

Angel investors, an angel syndicate, or a syndicate lead usually decide faster than venture capital — but they still have a thesis, and they still hate uncertainty. They’ll ask: do I understand the wedge, does the CEO communicate cleanly, and do I see a path where the equity I buy becomes meaningful for a future shareholder outcome (acquisition or IPO) with real liquidity? If the answer is “maybe,” many investors won’t commit.

5) How do I respond when investors won’t invest because they already invested in a competitor?

If investors won’t invest because they’ve already invested, that’s often a hard constraint tied to portfolio optics, reserves, and limited partners expectations. Your job isn’t to debate it — it’s to ask whether there’s any scenario where the conflict clears (different segment, different thesis angle, or a non-overlapping use case). If not, treat it as a clean no, protect your time, and keep the relationship warm for later when your traction changes the story and the means they need to re-evaluate.