This page explains how institutional capital evaluates real estate valuation and appraisal risk within commercial real estate and real estate financing decisions. It applies the universal capital decision logic defined at the institutional level, and expresses how that logic manifests specifically in real estate assets. Authority for capital allocation frameworks, portfolio construction, and allocator behavior remains with the upstream Hub 1 page. This page does not explain how to pitch, how to model returns, or how to structure transactions. It describes how evaluators, lenders, and investment committees interpret valuation signals, appraisal processes, and property risk when determining eligibility.

Real Estate Evaluation Context: Why Valuation Becomes the Primary Gate

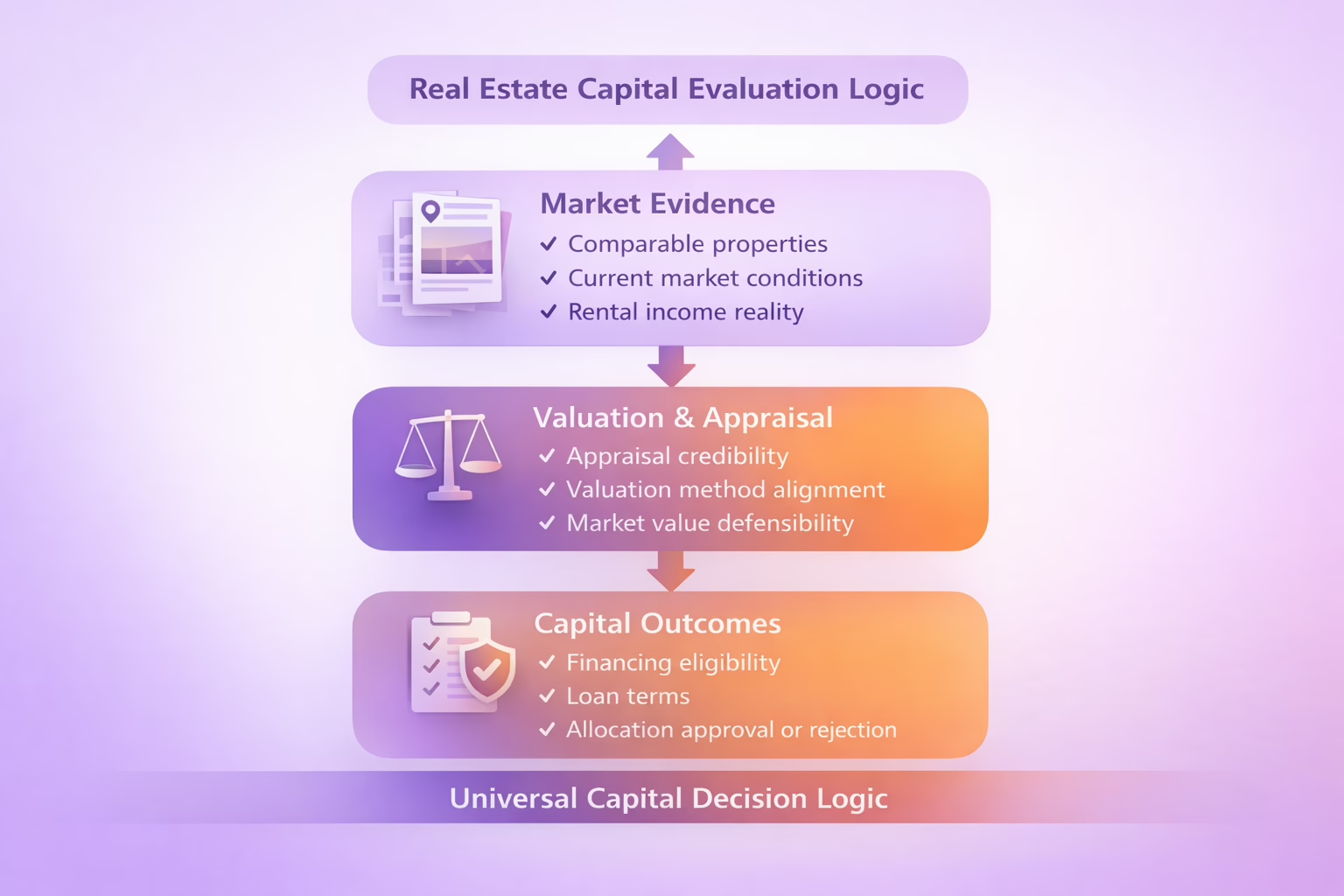

Real estate is constrained by immobility, capital intensity, and valuation subjectivity. Unlike operating companies, a real estate asset’s value is not inferred from growth optionality but anchored to current market value, income durability, and liquidation assumptions.

Institutional reviewers treat real estate investment as a balance-sheet asset first, not a narrative-driven opportunity. Valuation risk is non-linear: small shifts in market conditions, cap rates, or rental income can materially alter property value, loan coverage, and downside recovery. As a result, appraisal discipline and valuation method consistency become primary eligibility gates, not supporting evidence.

Appraisal Credibility and Valuation Independence

Institutional lenders and financial institutions require that real estate valuation be independently defensible. The appraiser is not evaluated for optimism, but for procedural compliance and conservatism.

This filter exists because real estate lending relies on collateral recovery under adverse market conditions. Reviewers look for alignment with recognized appraisal practice, use of appropriate valuation approaches, and adherence to professional standards of appraisal practice.

What typically fails here is valuation drift: appraisals that rely excessively on forward assumptions, selective comparable properties, or unsupported adjustments that inflate property value beyond defensible market data.

Valuation Method Selection and Property Type Alignment

Different property types require different valuation methods. Commercial property, rental property, and specialized real estate assets do not share interchangeable valuation logic.

Investment committees assess whether the valuation method reflects how the real estate market actually prices that asset. Income capitalization anchored to net operating income is evaluated differently than cost-based or sales comparison approaches. Automated valuation or simplified models are discounted where market complexity demands manual appraisal judgment.

Failure occurs when valuation methods are mismatched to property type or when multiple valuation approaches are presented without a clear reconciliation logic, creating ambiguity rather than confidence.

Income Durability and Cash Flow Verification

Rental income is not evaluated as potential upside but as current, defensible gross income. Reviewers examine whether cash flow assumptions align with current market conditions, lease structures, and tenant risk.

This filter exists because real estate financing depends on predictable debt service coverage. Lenders and allocators stress-test net operating income against vacancy, expense creep, and market softening.

What fails most often is reliance on future income normalization or optimistic stabilization narratives that are not yet reflected in actual cash flow.

Market Value Sensitivity and Comparable Evidence

Property valuation is anchored to local market evidence, not generalized real estate trends. Comparable properties, recently sold assets, and per-square-foot benchmarks are evaluated for relevance, not convenience.

Institutional reviewers assess whether the appraisal reflects the current market, including liquidity constraints and buyer behavior. Market analysis that smooths volatility or ignores recent market shifts raises immediate risk flags.

Failure appears when comparable properties are stale, geographically misaligned, or selectively chosen to support a predetermined property value.

Financing Structure and Valuation Containment

Real estate financing decisions integrate valuation directly into loan terms, leverage limits, and risk containment. Mortgage sizing, loan-to-value thresholds, and covenants are downstream expressions of valuation confidence.

This filter exists because valuation is the primary loss-absorption mechanism in real estate lending. When appraisal confidence is weak, capital does not reprice—it withdraws.

Common failure occurs when valuation assumptions and financing structures are misaligned, exposing lenders to downside scenarios that appraisal logic does not justify.

Sector-Specific Failure Modes in Real Estate Evaluation

Real estate funding is most commonly rejected for structural reasons rather than narrative weakness. These include inflated property value relative to market data, income projections unsupported by existing leases, appraisal processes that fail professional scrutiny, and valuation models that obscure downside risk.

These failures are not corrected through presentation, persuasion, or improved storytelling. They reflect fundamental evaluation breakdowns within real estate assets as capital instruments.

Role of Artifacts in Real Estate Evaluation

Pitch decks, valuation models, and appraisal services function as verification artifacts, not persuasion tools. They are used to confirm that property valuation, income assumptions, and market positioning align with institutional expectations.

These artifacts can validate consistency, methodology, and data integrity. They cannot alter market value, override appraisal discipline, or compensate for weak collateral fundamentals.

How Real Estate Expresses Universal Capital Logic

Real estate applies universal institutional capital logic through collateral primacy, downside containment, and valuation discipline. The same principles governing capital allocation, risk management, and portfolio alignment operate here, expressed through appraisal rigor and market value sensitivity rather than growth narratives.

At that point, real estate valuation risk is evaluated within the universal capital decision logic applied consistently across institutional asset classes.