Consumer brand capital evaluation is not about taste, creativity, or cultural relevance. It is about whether brand equity functions as a defensible capital asset—one that stabilizes cash flow, sustains margins, and reduces downside risk across cycles. This page explains how institutional capital evaluates consumer brands through that lens. It applies the universal capital decision logic established upstream, while isolating how brand-specific factors are interpreted inside investment committees. It does not explain how to build a brand, how to pitch, or how to persuade. Execution guidance lives elsewhere. Authority for capital logic remains upstream.

Sector Evaluation Context: Why Consumer Brands Are Treated Differently

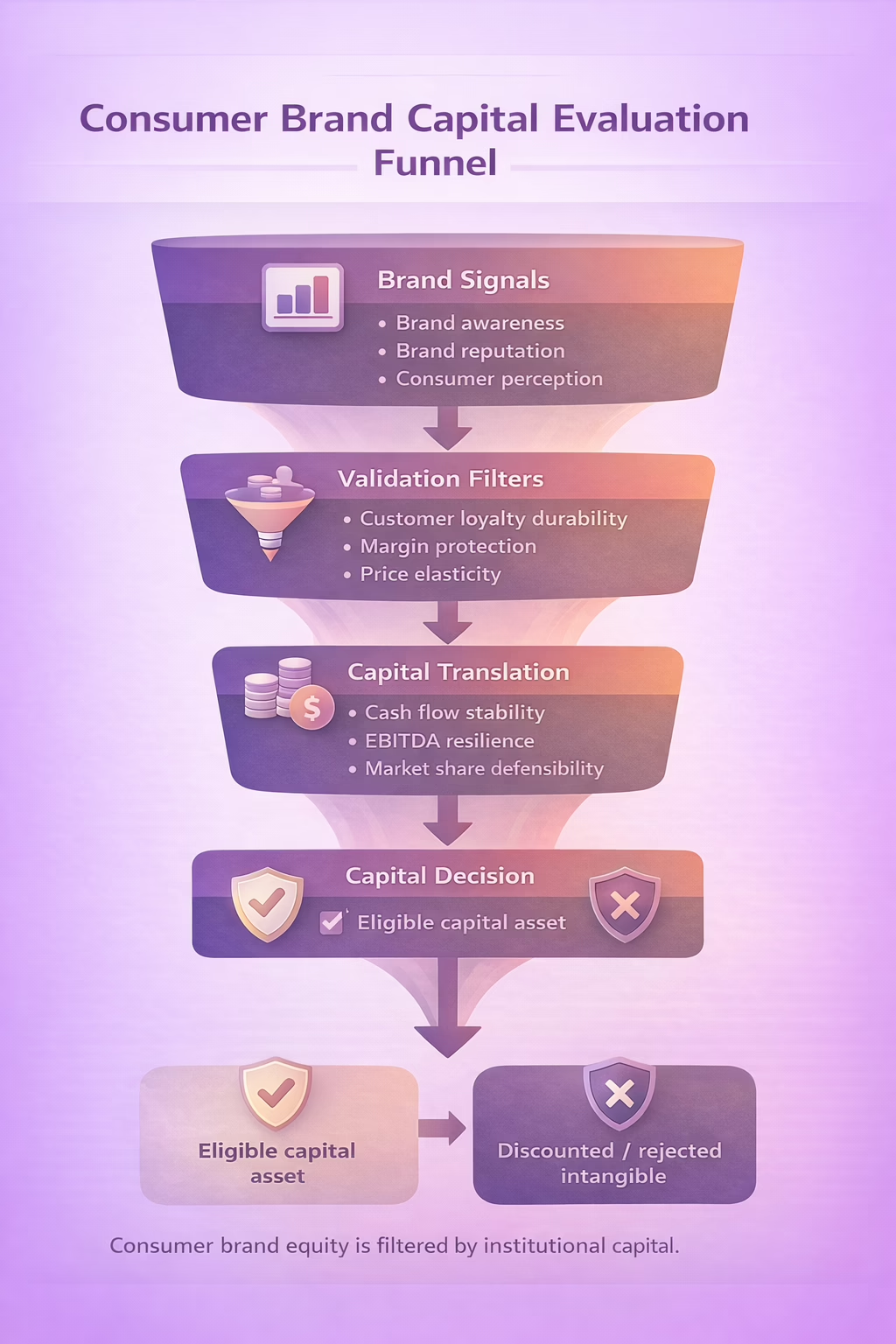

Consumer brands occupy an uncomfortable position in institutional portfolios. Their most valuable asset—brand equity—is intangible, difficult to measure, and heavily exposed to perception risk. Yet in mature consumer markets, brand value often explains pricing power, customer loyalty, and long-term profitability more reliably than short-term growth.

Capital treats this sector differently because risk is non-linear. A strong brand can compress customer acquisition costs, defend market share, and sustain EBITDA through downturns. A damaged brand can collapse faster than balance-sheet metrics suggest. Evaluation therefore focuses less on upside narratives and more on whether brand reputation behaves like a stabilizing capital asset under stress.

Brand Equity as a Capital Asset (Primary Evaluation Filter)

Investment committees first assess whether brand equity exists as a capitalizable asset, not a marketing claim. Brand awareness alone is insufficient. Reviewers look for evidence that brand recognition translates into repeat purchasing decisions, pricing resilience, and measurable customer loyalty.

What fails here is the assumption that brand value equals visibility. High social reach without durable brand associations signals volatility, not strength. Capital discounts brand equity that cannot be linked to sustained cash flow or that evaporates when promotional spend is reduced.

Measurement Credibility and Valuation Integrity

Because brand equity is difficult to quantify, reviewers scrutinize how it is measured, not just which metrics are presented. Net Promoter Score, brand metrics, and social media analytics are treated as directional signals, not valuation anchors.

What matters is whether qualitative and quantitative indicators are consistent with financial performance—profit margins, market share stability, and return on invested capital. Failure occurs when brand valuation relies on theoretical models or isolated metrics that do not reconcile with observed cash flow or capital efficiency.

Customer Loyalty and Margin Protection

Customer loyalty is evaluated as a margin defense mechanism, not a sentiment indicator. Institutional capital examines whether loyalty reduces price elasticity, lowers CAC over time, and sustains profitability as market conditions shift.

What typically fails is confusing customer satisfaction with switching resistance. Brands that require constant incentives to maintain volume are flagged as operationally fragile, regardless of reported loyalty scores or brand health surveys.

Brand Reputation and Downside Containment

Brand reputation is assessed through a downside lens. Reviewers ask whether reputational risk can be absorbed without impairing long-term value. This includes exposure to regulatory scrutiny, cultural volatility, and platform dependency.

Failure modes here are structural. Brands whose equity is concentrated in a narrow demographic, a single channel, or a transient consumer trend are treated as unstable. Capital does not assume reputational recovery unless history demonstrates it.

Sector-Specific Failure Modes in Consumer Brands

Consumer brand proposals are commonly rejected for structural reasons rather than poor storytelling. These include:

- Brand equity that cannot be separated from paid media spend

- Valuation assumptions that inflate intangible assets without cash-flow support

- Customer loyalty that collapses under price normalization

- Brand reputation exposed to single-event or platform-driven risk

- Margin profiles incompatible with long-term capital return expectations

No fixes are evaluated at this stage. These are gating conditions.

Role of Artifacts in Consumer Brand Evaluation

Pitch decks, brand valuation reports, and market research are treated as validation artifacts, not persuasion tools. They can substantiate consistency between brand perception, customer behavior, and financial metrics. They cannot convert weak brand equity into a capital asset, nor can they override structural risk.

Artifacts are used to test coherence. When brand narratives, metrics, and financials diverge, capital defaults to the most conservative interpretation.

Connection to Universal Capital Logic

Consumer brand evaluation is simply one expression of institutional capital’s universal logic: capital seeks assets that preserve value, control downside, and produce reliable returns. In this sector, brand equity substitutes for hard assets—but only when it demonstrably behaves like one.

The principles governing allocation, risk containment, and return expectations are not unique to consumer brands; they follow the same institutional screening logic defined in the institutional capital allocation framework, applied here through an intangible-asset lens.