Most founders think the pitch deck is for the pitch meeting.

It’s not.

Your deck lives a much longer, quieter life than you think. It gets screened by an associate on a Monday morning. It gets forwarded to a partner with a one-line Slack message. It gets projected on a conference room screen during an investment committee meeting where you’re not in the room and nobody’s going to ask you clarifying questions.

The deck has to work without you. And understanding how VCs actually evaluate it — at every stage of their internal process — is the difference between getting ghosted and getting a term sheet.

I’ve spent 13 years building pitch decks and watching them travel through this process. Here’s what actually happens on the other side of the table.

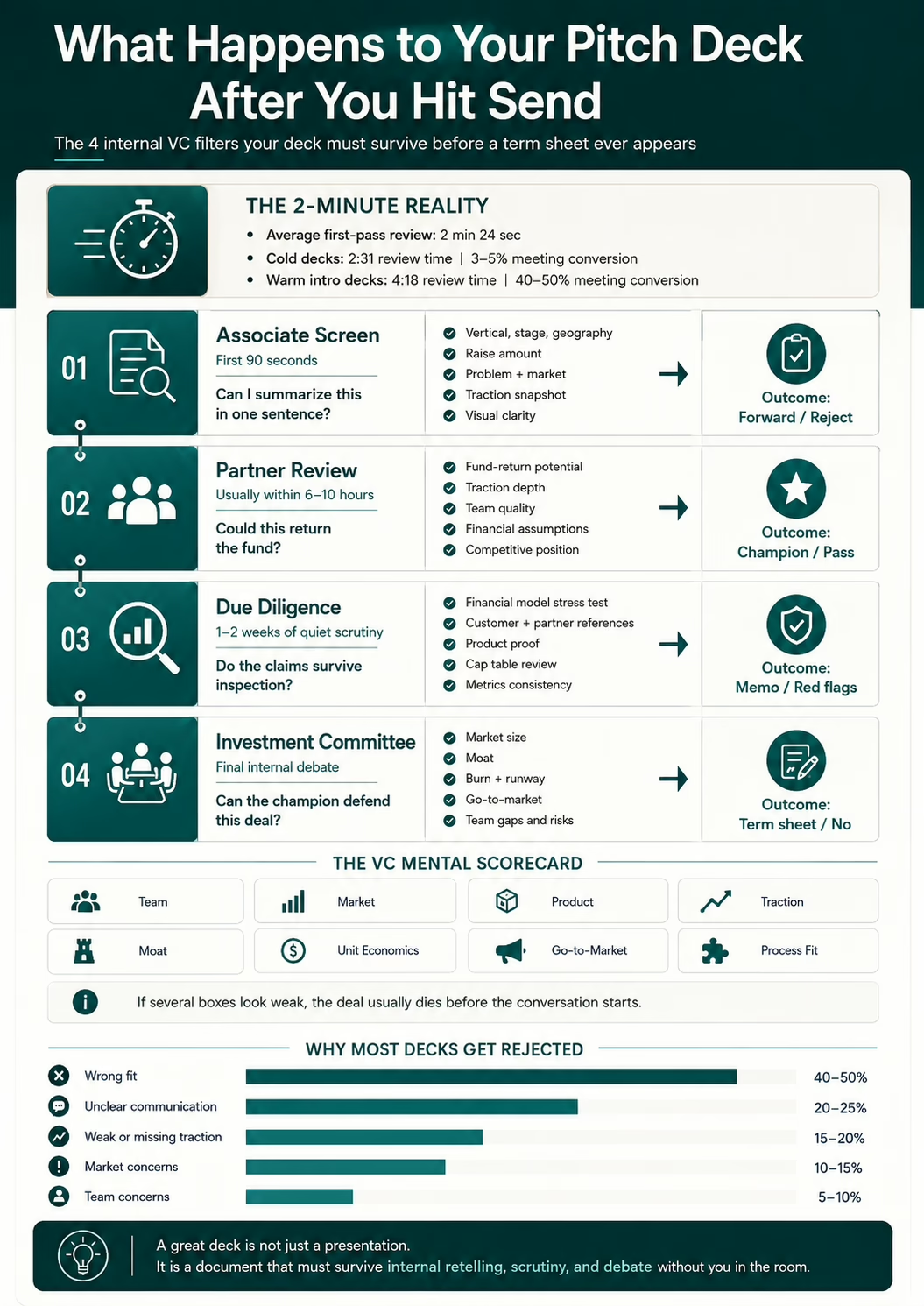

The 2-Minute Reality

Let’s start with the number that should terrify you: investors spend an average of 2 minutes and 24 seconds reviewing your pitch deck on first pass.

That’s down from 3 minutes 44 seconds in 2015. A 35% decline in a decade.

And it gets worse. Cold decks — the ones sent without a warm introduction — average 2 minutes 31 seconds and convert to meetings at 3-5%. Warm intro decks average 4 minutes 18 seconds and convert at 40-50%.

The gap isn’t just about time. It’s about attention quality. A cold deck gets scanned. A warm deck gets read. Same slides, radically different outcomes.

But here’s the thing most founders miss: that 2-minute window is just the first filter. Your deck goes through multiple evaluation stages, each with different criteria and different people making the call.

The VC’s Mental Scorecard (What They’re Actually Scoring)

Every experienced VC reads your deck while mentally filling in a scorecard. It’s not always written down, but the dimensions are consistent across firms. Here are the nine boxes they’re checking:

1. Team — Can these people actually execute this? Do they have domain expertise, relevant track records, and complementary skills? This is consistently the #1 or #2 factor in early-stage evaluation.

2. Market — Is this market big enough to return the fund? VCs aren’t looking for good businesses. They’re looking for businesses that can return 10x on their investment within their fund’s timeline.

3. Product — Does the solution actually solve the problem in a way that’s better, faster, or cheaper than alternatives? Is it defensible?

4. Traction — What evidence exists that this works? Revenue, users, pilots, LOIs, partnerships — anything that proves the market is pulling, not just the founder pushing.

5. Moat — What stops a well-funded competitor from copying this in 18 months? Network effects, proprietary data, regulatory advantages, switching costs.

6. Unit Economics — Do the numbers work at scale? CAC, LTV, margins, payback period. If the unit economics are broken at small scale, they’re not going to magically fix themselves at large scale.

7. Go-to-Market — How does this company actually acquire customers? A brilliant product with no distribution strategy is a hobby, not a business.

8. Risks — What could kill this? VCs assess risks internally even if you don’t put them in the deck. (And you shouldn’t. Don’t do the investor’s job for them.)

9. Process Fit — Does this match the fund’s thesis, check size, and stage focus? A perfect company that doesn’t fit the fund’s mandate is still a no.

The investment committee vote is essentially: “Do enough of these rows look strong?” If three or four dimensions are missing or weak, you’re dead before the conversation starts.

Stage 1: The Associate Screen (The First 90 Seconds)

Your deck doesn’t start with a partner. It starts with an associate or analyst who’s reviewing 20-50 decks per week. Their job is to filter, not to fall in love.

Here’s what they’re doing in those first 90 seconds:

Slides 1-2: Classification. What vertical? What stage? What geography? How much are they raising? If any of these don’t match the fund’s current focus, it’s over. No personal failing, no bad deck — just wrong fund. This is why knowing how to research VC funds before you pitch matters: you want to know the fund’s thesis, stage, geography, and check size before your deck ever lands in an associate’s inbox.

Slides 3-4: Problem and market. Is this a real problem or a solution looking for a problem? Is the market big enough to be interesting at this fund’s check size?

Quick scan of traction slide. Any revenue? Users? Pilots? At pre-seed, they’ll accept a strong team with a clear insight. At seed and beyond, they want numbers.

Visual gut check. This matters more than founders want to believe. A cluttered, text-heavy deck signals “this founder can’t communicate clearly.” A clean, structured deck signals competence. It’s not fair, but it’s real. Data suggests 10-20% of decks fail on design alone.

That’s also why pitch deck pricing varies so much. You’re not just paying for prettier slides — you’re paying for strategy, narrative clarity, financial logic, investor-ready structure, and design that doesn’t make an associate mentally close the tab. I break this down in more detail in this guide on how much a pitch deck costs.

The associate’s output is binary: forward to a partner, or don’t. They’ll attach a one-line summary: “Fintech play doing $40K MRR, interesting wedge into SMB lending, team from Stripe.” That’s your pitch now — one sentence from someone who spent 90 seconds with your deck.

This is why your opening slides need to do the heavy lifting. If the associate can’t retell your story in one sentence, you’ve already lost the internal game.

Stage 2: The Partner Review (Your Deck Presents Itself)

If an associate forwards your deck, a partner picks it up — usually within 6-10 hours. They’ll spend more time, but they’re reading with a different lens.

Partners are asking:

- “Is this a fund-returner?” — Not “is this a good business?” but “could this return the entire fund?” A $200M fund needs outcomes of $1B+. Most good businesses don’t qualify for venture capital. That’s not a criticism — it’s a filter.

- “Do I want to spend 4-6 weeks on due diligence?” — Partners have bandwidth for maybe 2-3 active deals at a time. Saying yes to your deal means saying no to another one.

- “Can I sell this internally?” — The partner who champions your deal has to convince their colleagues. They’re already thinking about how they’d pitch your company to their own investment committee.

The per-slide attention pattern here is bimodal and worth understanding. Partners either skim a slide in under 5 seconds or settle on it for 30-60 seconds. The smooth middle has thinned out.

What gets the 30-60 second treatment:

- Financial projections — not the hockey stick, but the assumptions. Revenue per customer, growth rate rationale, margin structure, burn rate.

- Team slide — included in 96% of top-performing decks.

- Traction/metrics — real numbers, not vanity metrics. MRR, retention, CAC payback.

- Competitive landscape — how you position against alternatives tells them how well you understand your market.

What gets skimmed in under 5 seconds:

- Mission statements

- Generic “About Us” content

- Slides with too much text (they literally skip them)

- Vague market size slides that just show a big TAM number without a bottom-up calculation

Stage 3: Due Diligence (1-2 Weeks of Quiet Scrutiny)

If a partner wants to move forward, the next phase is quiet and you often won’t know it’s happening. Over 1-2 weeks, the VC team will:

Stress-test your financials. They’ll rebuild your model from scratch — or at least the key assumptions. If your CAC is $50 and the industry average is $200, they’ll want to know why. If your churn is “2% monthly” but you only have 6 months of data, they’ll discount it heavily.

Run reference calls. They’ll talk to your customers, partners, and sometimes former employees. The questions aren’t “is this a great product?” — they’re “would you renew?” and “what almost made you not buy?”

Check your product. They’ll sign up, demo it, poke around. If the product experience doesn’t match the deck’s claims, that’s a red flag that’s very hard to recover from.

Review your cap table. Complex cap tables with too many small investors, unusual terms, or unclear ownership signal potential governance headaches.

Here’s the critical insight: during this phase, your deck is still the reference document. Partners flip back to it when writing up their investment memo. The numbers in your deck need to be accurate, consistent, and defensible — because they’re going to get checked.

Stage 4: The Investment Committee Vote

The IC meeting is where deals live or die, and you’re not in the room.

Your sponsoring partner has written an investment memo — typically a 2-5 page document that summarizes the opportunity, the risks, the deal terms, and why the firm should invest. Your deck is usually attached or embedded.

Other partners will challenge the thesis:

- “The market size seems aggressive — where did they get these numbers?”

- “What happens if [competitor] launches this feature?”

- “The burn rate gives them 14 months of runway — what if the next round takes longer?”

- “The team is strong technically but I don’t see a go-to-market leader.”

Your champion partner answers these using information from your deck, their due diligence, and conversations with you. Every unclear slide, every vague claim, every number without a source — these become ammunition for skeptical partners.

The vote typically requires consensus or near-consensus. One enthusiastic partner usually isn’t enough. One strongly opposed partner can often kill a deal.

This is why your deck needs to be a standalone document that answers objections before they’re raised. You’re not there to clarify. Your deck is.

The Five Slides That Decide Your Fate

Based on where investors spend their time and what IC meetings hinge on, these are the slides that matter most:

1. Traction / Metrics

This is the most scrutinized slide in your entire deck. Revenue, growth rate, retention, engagement — whatever your stage-appropriate metrics are, they need to be specific, honest, and impressive (or at least show a clear trajectory). Make sure you understand the specific metrics investors screen for at each stage so you’re highlighting the numbers that actually matter. Client logos make a massive impact here — they appear in 97% of top-performing decks. Recognizable names reduce perceived risk instantly.

2. Team

Investors back people, not just products. The team slide needs to answer: “Why are these the right people to build this specific company?” Domain expertise matters more than pedigree. A founder who spent 10 years in the industry they’re disrupting beats a Stanford MBA with no relevant experience, every time.

3. Business Model / Unit Economics

How do you make money? What are the margins? What does the path to profitability look like? In 2025/2026, “growth at all costs” is dead. VCs want to see that you understand the economics of your business and that they actually work.

4. Market Opportunity

Not just a big TAM number from a Gartner report. Show a bottom-up market sizing: “There are X potential customers, they’d pay Y per year, so our addressable market is Z.” This shows you actually understand your market instead of just Googling a big number.

5. The Ask + Use of Funds

What are you raising, and exactly what will it accomplish? “We’re raising $3M to reach $1M ARR by hitting these three things” is infinitely more fundable than “we’re raising $3M for growth.”

Why Most Decks Get Rejected (It’s Not What You Think)

The most common rejection reason isn’t a bad idea. It’s a bad fit.

Here’s the actual breakdown of why VCs pass:

Wrong fit (40-50% of rejections). Wrong stage, wrong sector, wrong geography, wrong check size. Nothing personal. Your deck could be perfect and still not match a fund’s mandate.

Unclear communication (20-25%). The VC couldn’t quickly understand what you do, who you serve, or why it matters. Remember: they have 2 minutes and 24 seconds. If you’re confusing at first glance, you’re gone.

Weak or missing traction (15-20%). Especially post-seed. “We’re pre-revenue but the market is huge” stopped working around 2022.

Market concerns (10-15%). Too small, too competitive, bad timing, regulatory risk.

Team concerns (5-10%). Missing key hires, no domain expertise, red flags from reference checks.

Notice what’s not on this list: design. Yes, a bad-looking deck hurts you. But design alone rarely kills a deal if the substance is there. It’s a multiplier, not a foundation.

How to Optimize Your Deck for the Internal Process

Now that you understand how the evaluation actually works, here’s how to build a deck that survives every stage:

Make it retellable in one sentence

The associate needs to forward it with a one-liner. The partner needs to pitch it to their colleagues. If your value proposition takes a paragraph to explain, simplify it.

Front-load the critical information

Slides 1-4 determine whether anyone reads slides 5-15. Problem, solution, traction, and market need to hit hard and fast.

Build a standalone document

Your deck travels without you. Every claim should be supported. Every number should have context. If a slide requires verbal explanation to make sense, it doesn’t work.

Include a clear next-step slide

Decks that end with “Let’s talk” or “Book a meeting” result in 22% more meetings than those that just… end. Tell the investor what you want them to do.

Prepare a data room

When diligence starts, you need to be ready within 24 hours. That means preparing a data room that survives diligence with your financial model, cap table, key contracts, customer list, product metrics. Delays during diligence signal disorganization.

Know your objections

Write down every reason a skeptical partner might argue against investing. Then make sure your deck addresses each one — not defensively, but proactively. Anticipating concerns signals maturity and self-awareness.

The Bottom Line

Your pitch deck isn’t a brochure. It’s a decision-making tool that travels through an institutional process with multiple stakeholders, each applying different filters at different stages.

The founders who understand this build decks that work in the room and outside of it. They build decks that survive the associate screen, the partner review, the due diligence, and the IC debate.

The ones who don’t? They build pretty presentations that tell a great story in person — and then die quietly in someone’s inbox when they can’t explain themselves.

Understanding the process doesn’t guarantee a yes. But it dramatically increases the odds that your deck gets a fair evaluation instead of a 90-second dismissal.

Need help building a pitch deck that actually survives the VC gauntlet? That’s what I do — get in touch.