What happens when your technology is genuinely impressive, technically defensible, and difficult to build, but investors still do not understand why they should care quickly enough?

That is one of the most frustrating problems deep tech founders face. You can spend years developing a product, proving a scientific principle, refining an engineering system, validating a model, building infrastructure, or solving a problem that most people in the room could not solve if you gave them a whiteboard, three espressos, and a week in the mountains. Then you sit down to pitch and realize that the actual investment conversation is not happening inside your technical reality. It is happening inside the investor’s mental model.

That mental model is different. Investors are not only asking whether the technology is impressive. They are asking whether the technology can become a company. They are asking whether the market is ready, whether the pain is urgent, whether the team can commercialize the solution, whether the risk is manageable, whether the timing makes sense, whether the capital required is justified, and whether the opportunity can become large enough to matter.

This is where many deep tech pitches fall apart. Not because the technology is weak. Not because the founder lacks intelligence. Usually, the opposite is true. The founder knows too much, cares too much about the mechanism, and explains from the inside out. The investor evaluates from the outside in.

That gap is the pitch problem.

A deep tech pitch deck should not dumb down the technology, because dumbing it down usually creates a vague story that makes the company look less serious. But it also should not force investors to swim through the full technical mechanism before they understand the investment case. The job is to translate technical complexity into investor conviction.

That translation is not cosmetic. It is not just better copywriting. It is not simply rearranging slides until the deck looks more “professional.” It is the strategic process of turning a difficult technical advantage into a story investors can understand, trust, evaluate, and repeat.

Because in fundraising, understanding is not a nice-to-have. It is oxygen.

Deep Tech Founders Are Usually Too Close to the Work

The biggest communication challenge for deep tech founders is proximity. Founders live inside the product, the science, the architecture, the workflow, the research, the engineering choices, the failed experiments, the breakthroughs, and the technical trade-offs that shaped the company. They know why the solution matters because they know what it took to get there.

Investors do not have that context yet.

That creates a painful imbalance. The founder is trying to explain the highest-value part of the company, while the investor is still trying to understand the basic shape of the opportunity. The founder wants to talk about the mechanism. The investor is still asking, “What problem is this solving, who urgently needs it, and why is now the right moment?”

This is why founders often mistake detail for clarity. They assume that if they explain enough technical detail, the investor will eventually see the value. Sometimes that works with highly technical investors who already understand the category. More often, it creates friction. The investor has to decode the product, infer the market, evaluate the commercial logic, and map the risk all at the same time.

That is too much work to put on the audience.

A good pitch does not make investors assemble the story themselves. It gives them a clear path into the complexity. It starts where the investor is, not where the founder is. This does not mean the technical depth disappears. It means the deck earns the right to go deeper by first establishing why the technology matters commercially.

A deep tech founder may think the breakthrough is the obvious starting point. But for the investor, the breakthrough becomes meaningful only when it is connected to a painful problem, a market shift, a credible wedge, a defensible advantage, and a believable path to value.

The hard truth is this: investors do not fund complexity just because it is complex. They fund the belief that a hard technical advantage can become a valuable business.

The Pitch Is Not a Technical Explanation. It Is an Investment Argument.

Many deep tech decks confuse explanation with persuasion. They explain what the company has built, how the technology works, what makes the system unique, and why the founder believes it is better. Those things matter, but they do not automatically create an investment argument.

An investment argument has a different structure. It shows why this company should exist, why this problem is worth solving now, why this solution has a meaningful advantage, why this team can execute, why the market will adopt it, why the risk is worth taking, and why this round of capital moves the company toward a more valuable state.

That is the difference.

A technical explanation says, “Here is what we built.”

An investment argument says, “Here is why this can become a fundable, valuable, defensible company.”

Deep tech founders often over-index on the first because that is where their confidence lives. They know the product. They know the science. They know the engineering. They can defend the mechanism. But an investor is not only buying the mechanism. The investor is buying a future company that does not fully exist yet.

That future company has to be made believable.

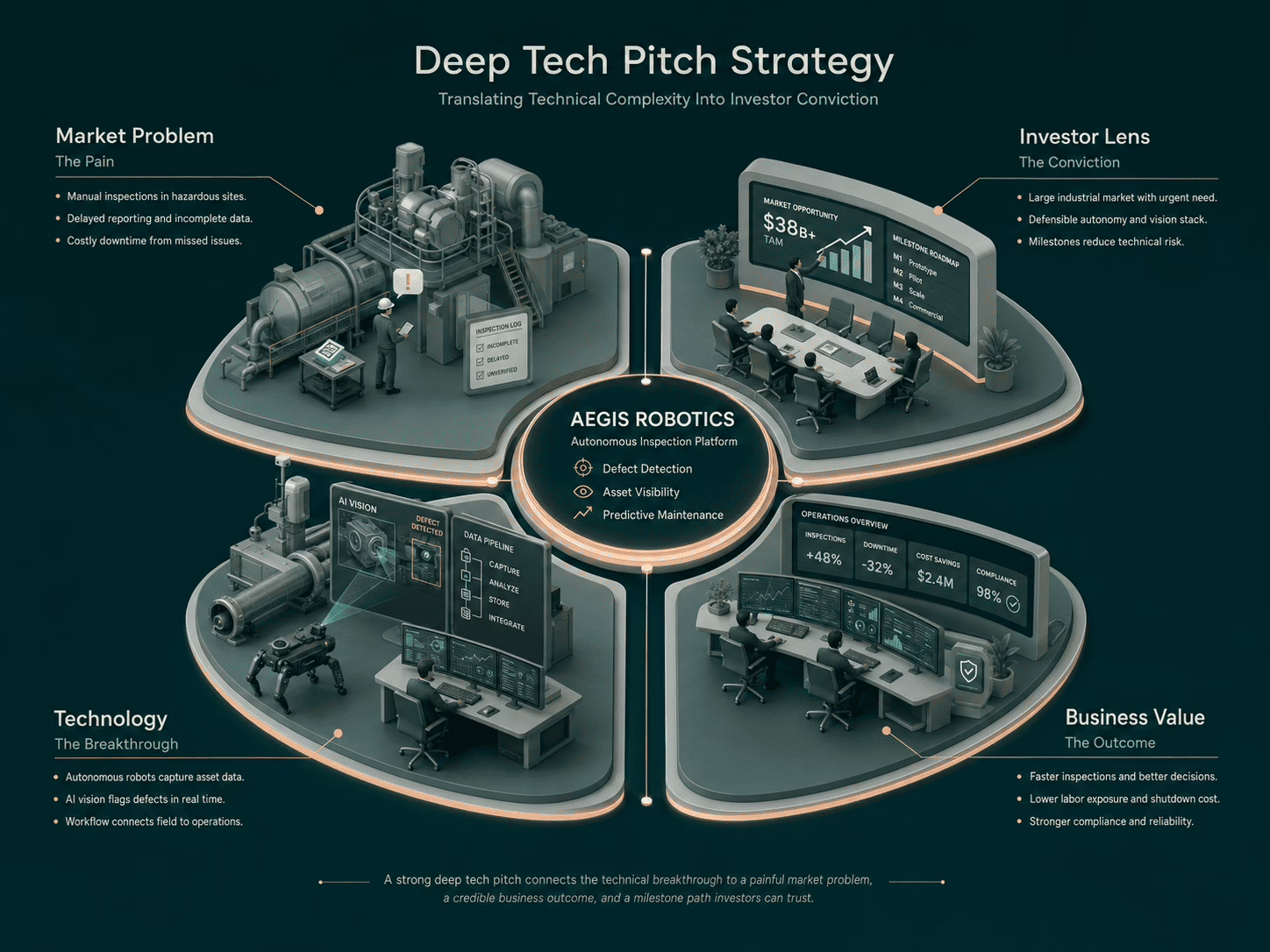

This is why the pitch deck has to translate across several dimensions at once. It has to translate the technology into a market problem. It has to translate the breakthrough into a business advantage. It has to translate uncertainty into milestones. It has to translate technical depth into defensibility. It has to translate founder expertise into investor confidence.

When those translations are missing, the deck may still look intelligent, but it does not move the investor. It becomes a technical document wearing a fundraising outfit.

And investors can smell that from three slides away.

The First Translation: From Technology to Market Pain

The first mistake deep tech founders make is opening with the technology before establishing the pain. This usually happens because the founder believes the technical breakthrough is the most impressive thing. It may be impressive, but the investor first needs to understand the world that makes the breakthrough necessary.

A robotics founder might want to begin with the autonomy stack, sensor fusion, hardware design, or navigation system. But the investor first needs to understand the painful reality of the customer: dangerous inspection environments, labor shortages, high downtime, inconsistent manual processes, or expensive operational failures.

A biotech founder might want to begin with the mechanism of action. But the investor first needs to understand the clinical need, the limitations of current treatments, the patient population, the regulatory path, and the commercial opportunity.

An AI infrastructure founder might want to begin with the model architecture or system performance. But the investor first needs to understand the operational bottleneck, the cost of current workflows, the reliability issue, or the scale problem that makes the technology valuable.

The mechanism becomes interesting after the pain is clear.

This is not about making the deck simplistic. It is about creating emotional and commercial context. Pain gives the investor a reason to care. Without it, the technology floats in space, impressive but unattached to urgency.

A strong deep tech pitch should define the problem in the buyer’s world before introducing the technical solution. The problem should feel concrete. It should not be a vague statement like “current systems are inefficient.” That is not pain. That is a foggy complaint. A stronger problem statement shows the operational, financial, strategic, or human consequence of the issue.

For example, instead of saying, “Industrial inspection processes are inefficient,” a stronger framing would be: “Industrial operators still rely on manual inspections in high-risk environments, creating long shutdown windows, safety exposure, delayed reporting, and expensive maintenance decisions based on incomplete visibility.”

Now the investor has a world. The technology has somewhere to land.

The Second Translation: From Breakthrough to Business Advantage

Once the problem is clear, the founder has to explain what the technical breakthrough makes possible. This is where many pitches still stay too technical. They describe the innovation, but they do not translate it into a business consequence.

A breakthrough matters because of what it changes.

Does it reduce cost? Does it unlock a new workflow? Does it improve performance by a meaningful margin? Does it make deployment easier? Does it shorten time to value? Does it reduce risk? Does it create a defensible advantage? Does it make something commercially possible that was previously impractical?

That is the language investors need.

A founder might say, “Our proprietary model improves data interpretation across fragmented operational environments.” That may be true, but it does not yet explain why the investor should care. A more investor-useful version would be: “Our system turns fragmented operational data into reliable decision signals, reducing manual review time and helping teams act before small issues become expensive failures.”

The technical capability is still there, but now it is connected to an outcome.

This translation matters because investors are constantly evaluating whether the company’s technical edge creates a meaningful business edge. A small technical improvement can be interesting, but not necessarily fundable. A technical improvement that changes cost structure, adoption speed, risk profile, performance, or market access becomes more compelling.

Deep tech founders need to be careful here. The pitch should not overclaim. Investors are allergic to hand-wavy “revolutionary” statements, especially in technical categories where diligence will eventually expose exaggeration. The goal is not to inflate the breakthrough. The goal is to explain its consequence clearly.

A useful way to think about this is: “Because we can do X technically, the market can now do Y commercially.”

That sentence forces the pitch to connect the mechanism to value.

The Third Translation: From Risk to Milestones

Deep tech investors expect risk. They know the company may face technical risk, manufacturing risk, regulatory risk, adoption risk, scientific risk, integration risk, capital intensity, or long sales cycles. Pretending those risks do not exist does not make the deck stronger. It makes the founder look naive.

The better move is to frame risk intelligently.

A strong deep tech pitch does not say, “There is no risk.” It says, “Here is what has already been proven, here is what remains uncertain, and here is how this round of capital reduces the next major risks.”

That is a more mature conversation.

This is especially important because deep tech fundraising is often milestone-driven. Investors want to understand what the next round of capital unlocks. They want to know what will be true after this round that is not true today. They want to see how technical validation connects to commercial progress.

A weak use-of-funds slide says the money will go toward product development, hiring, marketing, and operations. That is technically an answer, but it is not an investment argument. A stronger version ties the raise to value-creating milestones: completing prototype v2, securing three paid pilots, validating performance in field conditions, submitting regulatory documentation, reducing unit cost, hiring a key technical lead, or converting LOIs into commercial contracts.

Each milestone should reduce uncertainty.

This is how founders turn risk into a roadmap. The investor does not need every risk removed today. They need to believe the founder knows which risks matter, which ones have been reduced, which ones come next, and why the requested capital is the right amount to move the company forward.

That kind of clarity builds trust. It shows the founder understands the business, not just the technology.

The Retellability Test

One of the most overlooked parts of pitch strategy is retellability.

Your pitch does not only have to work while you are presenting it. It has to work after you leave the room. It has to survive being forwarded, summarized, discussed, challenged, and compared against other opportunities. An associate may need to explain it to a partner. A partner may need to explain it in an investment meeting. Someone may need to summarize it after reading the deck without you there to add context.

If the story collapses without the founder in the room, the deck is not doing enough work.

This is why the company needs a clear one-sentence investment narrative. Not a tagline. Not a slogan. A repeatable explanation of what the company does, who it helps, and why it matters.

For example: “We help industrial operators automate high-risk inspections using autonomous robotics, reducing downtime and human exposure in environments where manual work is slow, dangerous, and expensive.”

That sentence is not trying to explain everything. It gives the investor a handle. It creates a clean mental file. The details can follow.

Deep tech founders sometimes resist this because they feel one sentence cannot capture the full sophistication of the company. That is true. It cannot. That is not its job. Its job is to create an entry point.

A pitch needs different levels of explanation. The one-liner creates access. The problem slide creates urgency. The solution slide creates clarity. The how-it-works slide creates credibility. The proof slide reduces doubt. The moat slide explains defensibility. The milestone slide explains fundability.

When those levels are sequenced properly, investors can follow the story without drowning in it.

The Visual Problem: Looking Technical Is Not the Same as Looking Credible

Deep tech decks also struggle visually because founders often assume that a technical company should look “techy.” That usually leads to the same tired visual language: blue gradients, glowing lines, floating dashboards, abstract AI heads, circuit-board backgrounds, cloud icons, 3D cubes, and stock imagery that looks like innovation was rendered by a laptop having a fever.

The problem is not that these visuals are always ugly. Some are polished. Some even look expensive. The problem is that they are generic. They communicate the broad category of “technology” without communicating the specific intelligence of the company.

That is dangerous for deep tech because specificity is the entire point.

If a robotics company looks like a generic SaaS dashboard, the pitch loses physical-world credibility. If a biotech company looks like a wellness startup, the pitch loses scientific seriousness. If an infrastructure company looks like a trendy AI tool, the pitch loses operational weight. If a climate hardware company looks like a generic green tech landing page, the pitch loses its engineering edge.

The visual identity of the deck should support the argument.

That does not mean over-designing. In fact, deep tech decks often benefit from restraint. The goal is not to decorate the complexity. The goal is to clarify it.

A strong deep tech deck uses visual language that comes from the company’s actual world: system maps, architecture diagrams, process flows, technical annotations, evidence-led charts, product schematics, operational diagrams, milestone roadmaps, before-and-after comparisons, and clean hierarchy. These elements do more than make the deck look credible. They help investors understand the company faster.

Design becomes part of the explanation.

A good diagram can reduce confusion. A good comparison can make the old world and new world obvious. A good milestone roadmap can make a risky company feel more structured. A good technical architecture slide can show sophistication without becoming a wall of jargon.

That is what pitch design is supposed to do.

How to Structure a Deep Tech Pitch Deck

A deep tech pitch deck should not blindly follow a generic startup deck structure. The usual sections still matter, but the emphasis changes because the investor needs to understand both the technical advantage and the path to commercialization.

The opening should establish the investment thesis, not a vague mission statement. A sentence like “Autonomous inspection for high-risk industrial sites where manual work is slow, dangerous, and expensive” is much stronger than “Revolutionizing the future of industrial intelligence.” The first one creates a market, a problem, and a reason to care. The second one sounds like it escaped from a conference lanyard.

The problem section should make the customer pain concrete. Investors should be able to feel the operational, financial, regulatory, or strategic consequence of the problem. If the pain is too abstract, the solution will feel optional.

The why-now section is especially important in deep tech. Investors need to know why this can work now and why the market is ready now. Maybe costs have changed. Maybe regulation has shifted. Maybe compute, materials, sensors, manufacturing, distribution, or customer behavior has reached a tipping point. Without a strong why-now argument, deep tech can easily sound too early.

The solution section should introduce the product in plain language before going deeper into the mechanism. The founder should explain what the product does, who uses it, and what changes because it exists. The detailed technical explanation belongs after that foundation is established.

The how-it-works section should create credibility without overloading the investor. This is where diagrams matter. A clear technical flow can show sophistication without requiring the investor to read a small novel disguised as a slide. The deck should show enough depth to build confidence, while leaving the deepest technical material for the appendix, data room, white paper, demo, or diligence process.

The moat section should explain why the company is difficult to copy. “Proprietary technology” is not enough. Everyone says that, including companies whose proprietary technology is basically a spreadsheet with confidence. The deck needs to explain what is defensible: IP, data, technical know-how, manufacturing process, regulatory progress, integration complexity, deployment learning, partnerships, cost advantage, or some combination of those.

The proof section should reduce doubt. This is where the founder shows what has already been validated: prototype results, pilots, benchmarks, customer interest, letters of intent, paid deployments, regulatory progress, patents, peer-reviewed work, technical milestones, or early revenue. The proof does not need to remove all risk, but it should make the company feel real.

The market section should avoid lazy TAM theatrics. A huge market is not enough. Investors need to understand the wedge: who buys first, why they buy first, and how that initial market expands into something larger. Deep tech often needs a specific beachhead because adoption can be slow, complex, or trust-dependent.

The business model section should explain how this becomes a company, not just a project. Is it hardware sales, recurring software, licensing, usage-based revenue, service plus platform, enterprise contracts, consumables, data products, or some hybrid model? Deep tech business models can be more complex than pure SaaS, so clarity matters.

The go-to-market section should be practical. “Strategic partnerships” is not a plan by itself. It is a phrase wearing a suit. The deck should explain who the first buyer is, who influences the buying decision, what proof they need, how the pilot works, what adoption friction exists, and how the company expands after the first deployment.

The milestones and use-of-funds section should connect the raise to risk reduction. This is where deep tech decks can become much stronger than generic decks. The investor should understand exactly what the capital unlocks and how those milestones increase company value.

The team section should prove that the company can execute both technically and commercially. Deep technical expertise is necessary, but not always sufficient. If the founding team is heavily technical, the deck should show how commercial, regulatory, manufacturing, or go-to-market gaps are being addressed through hires, advisors, partners, or planned use of funds.

Finally, the ask should feel connected to the entire story. The amount being raised, the runway, the milestones, and the next financing event should all make sense together. The ask should not feel like a random number placed at the end of the deck because someone said decks need an ask slide.

The Founder’s Real Job in the Pitch

The founder’s job is not to prove they are the smartest technical person in the room. They might be, but that alone does not close a round.

The founder’s job is to make the investor believe that the company has found a valuable problem, built or is building a credible solution, understands the risks, has a plan to reduce those risks, and can turn a technical advantage into a commercial outcome.

That is a very different job.

It requires restraint. It requires sequencing. It requires deciding what not to say yet. It requires accepting that the investor does not need the full technical explanation before understanding the opportunity. It requires building a pitch that guides the investor from curiosity to conviction.

Deep tech founders often worry that simplifying the pitch will make them look less serious. Usually, the opposite happens. A clear pitch makes the founder look more in control. It shows that they understand not only the product, but the market, the buyer, the investor, and the path ahead.

Confusion does not signal sophistication. It signals work left undone.

Common Deep Tech Pitch Mistakes

One of the most common mistakes is starting with the technology instead of the problem. This makes the deck feel like a technical presentation rather than an investment case. The investor should understand the pain before being asked to appreciate the mechanism.

Another mistake is treating technical detail as proof by default. Detail can create credibility, but only when it is organized around the investor’s questions. A dense slide full of technical explanation may impress a specialist, but it may also confuse a generalist investor who still needs to understand the business logic.

A third mistake is using generic tech visuals. If the deck looks like every SaaS company, AI tool, or cloud platform, it weakens the company’s specificity. Deep tech brands need visual language that reflects their actual category, not generic “future of technology” wallpaper.

Another mistake is hiding risk. Investors already know risk exists. A founder who frames risk clearly and connects it to milestones often appears more credible than one who pretends everything is solved.

A fifth mistake is relying on a huge market slide without explaining the wedge. A massive market is not persuasive unless the deck explains how the company enters it, who buys first, why they buy, and how the opportunity expands.

The final mistake is failing the retellability test. If the investor cannot explain the company after reading the deck, the pitch is too dependent on the founder. That is a problem because investment decisions rarely happen only in the founder’s presence.

Final Thought

Deep tech founders do not need to make their companies sound less technical. They need to make the technical value easier to understand, trust, evaluate, and repeat.

That is the real job of the pitch deck.

The deck should not show everything the founder knows. It should not bury the investment case under the mechanism. It should not confuse technical depth with investor clarity. It should translate.

It should translate technology into market pain, breakthrough into business advantage, uncertainty into milestones, complexity into confidence, and founder expertise into investor conviction.

Because investors do not fund complexity just because it is complex.

They fund the belief that a difficult technical advantage can become a valuable business.

Your pitch has to build that belief before the technical brilliance can fully matter.