Real estate is a $380 trillion asset class. PropTech — the technology layer reshaping how we build, buy, sell, manage, and finance property — is now a $53 billion market growing at nearly 18% annually. And yet, most PropTech pitch decks I review look like they were written by founders who’ve never sat across from a real estate investor.

Here’s the problem: real estate investors and traditional tech VCs evaluate opportunities through fundamentally different lenses. A SaaS playbook that works beautifully for an HR-tech startup lands flat with someone whose frame of reference is transaction volume, broker margin, and regulatory exposure.

I’ve worked with PropTech founders across every subcategory — property management platforms, construction tech, RE fintech, building operations, leasing automation. The ones who raise successfully aren’t just building great products. They’ve learned to translate technology value into the language that real estate capital actually speaks.

This guide walks through every slide of a PropTech pitch deck, with the specific framing, metrics, and positioning that real estate-literate investors expect to see.

First: Know Which PropTech Category You’re In

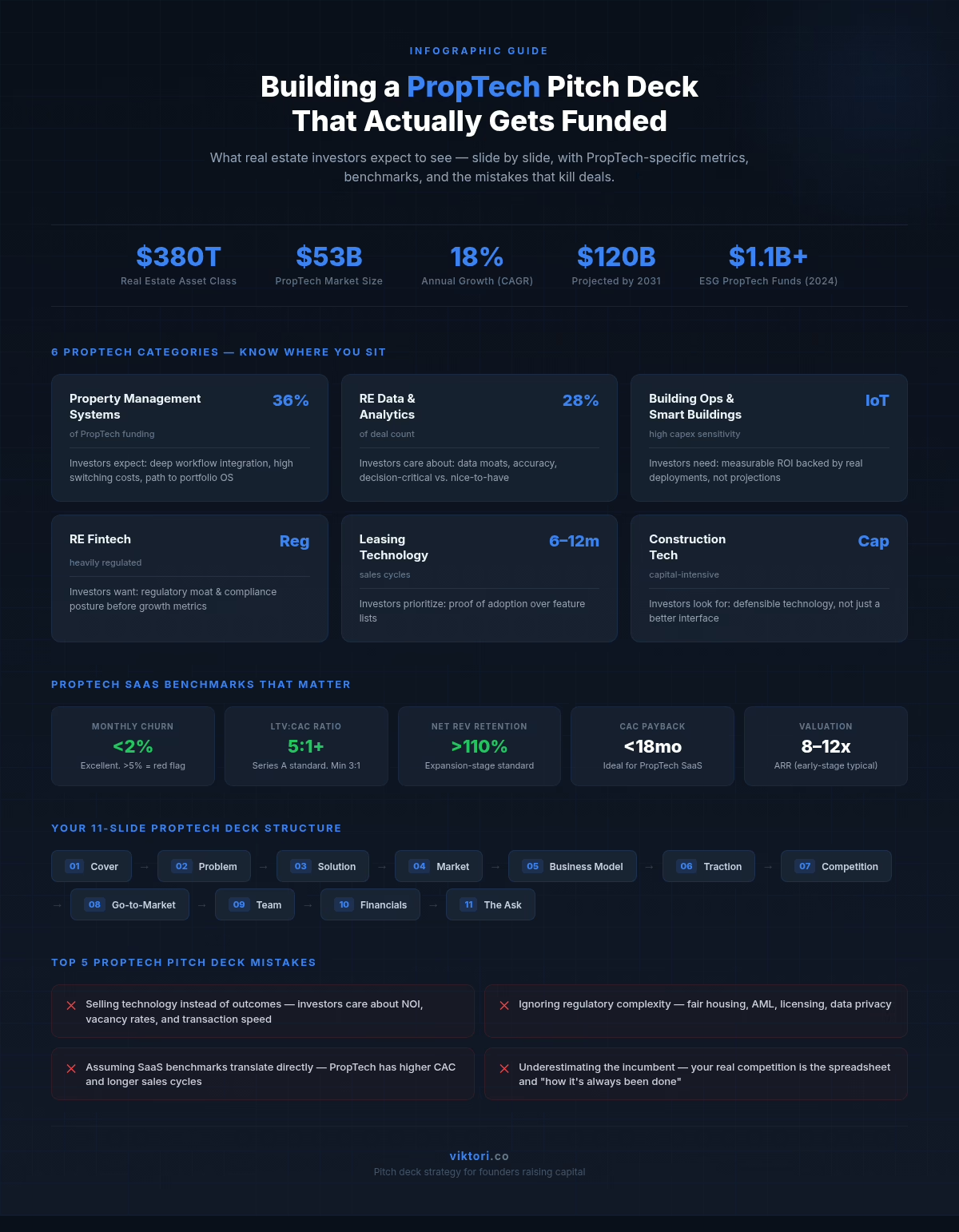

Before you touch a single slide, get precise about where you sit. PropTech is not one market — it’s at least six, and each has different investor expectations:

Property Management Systems — The largest category by capital raised (roughly 36% of PropTech funding). Investors expect deep workflow integration, high switching costs, and a path to becoming the operating system for property portfolios. Examples: EliseAI ($250M Series D from a16z), MagicDoor, Buildium.

Real Estate Data & Analytics — The most active category by deal count (~28% of deals). Investors care about data moats, accuracy, and whether you’re a nice-to-have dashboard or a decision-critical tool. Examples: Lumoview, Cohabit.

Building Operations & Smart Buildings — IoT, energy management, building automation. High capex sensitivity. Investors need to see measurable ROI — the “cut operating costs by 30%” story needs to be backed by real deployments. Examples: Runwise ($30M Series B), aedifion, viboo.

RE Fintech — Mortgage tech, crowdfunding platforms, transaction infrastructure. Heavily regulated. Investors want to understand your regulatory moat and compliance posture before they care about growth.

Leasing Technology — Automating the tenant lifecycle. Long enterprise sales cycles. Proof of adoption matters more than feature lists.

Construction Tech — Project management, prefab, materials marketplace. Capital-intensive by nature. Investors are looking for defensible technology, not just a better interface on top of existing processes.

Your category dictates your metrics, your competitive framing, and your go-to-market story. Don’t build a generic pitch deck and hope it lands.

Slide 1: The Cover — Set the Right Frame

Your cover slide needs to communicate three things instantly: what you do, who it’s for, and why now.

The mistake most PropTech founders make here is leading with technology language. “AI-native transaction software” says nothing to a real estate investor. “The operating system for modern property management” immediately tells them where to file you mentally.

Opendoor’s Series A cover said “Liquidity for Residential Real Estate.” Four words. A real estate investor reads that and immediately understands the value proposition, the market, and the problem being solved. That’s the bar.

What to include:

- Company name and logo

- One-line positioning statement in real estate language, not tech language

- Funding round context (Series A, Seed, etc.)

- A clean visual that signals “real estate” without being generic

Slide 2: The Problem — Speak the Operator’s Language

Real estate operators still rely heavily on legacy tools, spreadsheets, and offline processes. Introducing new technology means changing workflows that have worked (badly, but consistently) for decades. Your problem slide needs to feel like you’ve lived inside these workflows.

Generic problem statements kill PropTech decks. “The real estate industry is inefficient” — sure, everyone knows that. What specifically? Which workflow? Which stakeholder? What does it cost them?

Strong problem framing for PropTech:

- Quantify the cost of the status quo (“The average property manager spends 14 hours/week on manual tenant communication — that’s $32,000/year per manager in labor alone”)

- Name the specific pain point by stakeholder (brokers care about commission splits, property managers care about maintenance response time, developers care about permitting delays)

- Acknowledge that your buyer has been burned by tech promises before — this builds credibility

Avoid:

- Industry-level statistics without connecting them to your specific user

- “Real estate is the largest asset class” — investors know this; it’s not a problem statement

- Implying your buyers are backward for not adopting technology — they have rational reasons for caution

Slide 3: Your Solution — Technology With Distribution Logic

Here’s where most PropTech decks lose the plot. They demo features. Investors don’t fund features — they fund distribution advantages.

Real estate has a peculiar dynamic: buyers evaluate vendors through transaction volume and peer networks, not product demos. If your solution can’t demonstrate how it fits into existing workflows (at least initially), it doesn’t matter how elegant the technology is.

What to show:

- Your product in context — screenshots of the actual interface solving the actual problem

- The “wedge” — how you get into the first account without requiring a complete workflow overhaul

- Integration points with existing tools (MLS systems, building management systems, accounting software — whatever your user already runs)

- A 30-second explainer of how it works: input → process → output, in plain language

The critical framing: Position your technology as infrastructure, not an add-on. The companies that raise the most in PropTech are the ones that become essential to daily operations — not the ones that are nice to have during quarterly reviews.

Slide 4: Market Opportunity — Get Granular

The PropTech market is projected to reach $120 billion by 2031. That number is useless in your deck unless you can draw a straight line from it to your actual revenue opportunity.

Real estate investors are trained to be skeptical of top-down market sizing. They deal in specific geographies, specific property types, specific transaction sizes. Your market slide should reflect that discipline.

Strong PropTech market framing:

- TAM: The total PropTech market relevant to your category (not the entire real estate market)

- SAM: The segment you can realistically serve with your current product and go-to-market

- SOM: Your actual target for the next 18-24 months, with the math to back it up

If you’re a building operations platform focused on commercial office buildings in Tier 1 US cities, say that. Don’t claim the entire smart building market as your TAM.

What investors want to see:

- Market sizing tied to your unit economics (“There are 47,000 commercial property management companies in the US; our SOM is the 3,200 that manage portfolios of 500+ units”)

- Growth drivers that are structural, not cyclical (ESG mandates, regulatory changes, demographic shifts)

- Where capital is flowing — PropTech funding in 2025 was heavily concentrated in property management systems and building operations. If you’re in a hot subcategory, lean into it

Slide 5: Business Model — Show How Money Moves

PropTech business models are more varied than typical SaaS, and investors need to understand exactly how you monetize.

Common PropTech models and what investors look for in each:

| Model | Key Metric | Investor Focus |

|---|---|---|

| SaaS (per-unit/property) | ARR, net rev retention | Expansion as portfolios grow |

| Marketplace/transaction | GMV, take rate | Liquidity, network effects |

| Managed service | Rev/property, margin | Scalability w/o headcount |

| Data/analytics | Seats or API calls | Data moat, switching costs |

If you’re SaaS, show pricing per unit, per seat, or per property. Show how revenue grows as customers add properties to their portfolio — this is the expansion revenue story that real estate investors love, because portfolio growth is built into how the industry works.

If you’re transaction-based, show the transaction flow, your take rate, and how you achieve liquidity on both sides.

Important: Be explicit about whether you’re capital-light (pure software) or capital-intensive (iBuying, construction, hardware). This fundamentally changes the investor profile you should be targeting and the metrics they expect.

Slide 6: Traction — Real Estate Metrics, Not Vanity Metrics

In PropTech, traction means something specific. It’s not app downloads or website visits. It’s:

- Units under management (for property management platforms)

- Transaction volume (for marketplaces and fintech)

- Square footage deployed (for building operations and IoT)

- Properties connected (for data platforms)

- Revenue and growth rate (always)

PropTech SaaS benchmarks investors compare you against:

- Monthly churn: Below 2% is excellent, 2-3.5% is acceptable, above 5% is a red flag

- CAC: $50-$10,000 depending on segment (enterprise higher, SMB lower)

- LTV: $800-$100,000 depending on customer size

- LTV:CAC ratio: 3:1 minimum, 5:1+ for Series A

- Net revenue retention: Above 110% is the standard for expansion-stage PropTech SaaS

If you have pilot deployments with recognizable property companies, name them. Real estate is a relationship-driven industry — logos carry unusual weight.

One nuance: PropTech sales cycles are long, often 6-12 months for enterprise deals. If you’re early-stage, investors understand this. But you need to show pipeline, LOIs, or paid pilots to prove the demand exists beyond conversations.

Slide 7: Competitive Landscape — Don’t Ignore the Incumbents

PropTech founders routinely make the mistake of only comparing themselves to other startups. Your real competition is often a spreadsheet, a phone call, or a property manager who’s been doing things the same way for 20 years.

Position your competitive slide around:

- The status quo (manual processes, legacy systems) as competitor #1

- Horizontal SaaS tools being used off-label (Salesforce, Excel, custom Access databases)

- Direct PropTech competitors

- Adjacent platforms that might expand into your space

Don’t claim “no competition.” In real estate, there’s always an alternative — even if it’s deeply inefficient. Investors who know the industry will immediately discount your credibility if you pretend otherwise.

Show your moat explicitly. In PropTech, defensible advantages typically come from:

- Data network effects (more properties → better analytics → more properties)

- Integration depth (once your platform is wired into a building’s BMS, switching costs are real)

- Regulatory compliance (if you’ve solved licensing, AML, or fair housing compliance, that’s a barrier competitors face too)

- Distribution partnerships (exclusive relationships with property management associations, brokerage networks, or REITs)

Slide 8: Go-to-Market — Prove You Understand the Buyer

This is where most PropTech decks either earn trust or lose the room.

PropTech buyers don’t respond to inbound marketing the way SaaS buyers in other verticals do. They evaluate vendors through transaction volume, peer referrals, and industry events. Your go-to-market needs to reflect this reality.

What works in PropTech GTM:

- Channel partnerships with property management associations, brokerage networks, or MLS providers

- Land-and-expand within portfolio companies (one property → entire portfolio)

- Strategic relationships with REITs, institutional owners, or housing authorities

- Industry conference presence (NMHC, NAA, ICSC, RealComm, CREtech)

- Referral networks — real estate runs on relationships more than any other industry

What doesn’t work:

- “We’ll run Google Ads and do content marketing” — this works for awareness, not for closing $50K+ annual contracts

- Product-led growth assumptions in a market where decisions involve legal review, procurement cycles, and committee approvals

- Ignoring regional market dynamics — real estate is intensely local, even when the technology is national

Slide 9: Team — Show Real Estate DNA

The question investors ask about PropTech teams isn’t just “can they build the product?” It’s “do they understand the industry well enough to sell into it?”

The best PropTech teams have at least one person who’s worked inside the real estate industry — not just studied it. Someone who’s managed properties, brokered deals, or built for this market before. If you have that, make it prominent.

What to highlight:

- Real estate operating experience (years, transaction volume, portfolio size managed)

- Technical capabilities relevant to your specific challenge

- Previous startup experience or track record

- Advisors or board members with deep real estate networks

If your team is all tech and no real estate experience, address it directly. Show your advisory board, your early customers who serve as de facto advisors, or your domain expert hires. Don’t leave investors to wonder whether you understand the market.

Slide 10: Financials — Build for Real Estate Economics

PropTech financial projections need to account for the realities of real estate sales cycles and deployment timelines. Don’t project SaaS-typical ramp times if your average deal takes 9 months to close.

What investors want to see:

- Revenue projections for 3-5 years with clear assumptions

- Unit economics by customer segment

- CAC payback period (ideally under 18 months for PropTech SaaS)

- Path to profitability or clear rationale for continued investment

- Use of funds tied to specific milestones

One thing I see constantly: Founders projecting 30% month-over-month growth in a market where enterprise deals close on quarter-long timelines. If your projections don’t match the buying behavior of your market, investors notice immediately.

Build a bottoms-up model: number of target accounts × conversion rate × average contract value × expansion rate. This shows you understand your market at a granular level.

Slide 11: The Ask — Be Specific About Capital Deployment

State your raise amount, your target valuation range (if you’re comfortable sharing it), and exactly how the capital will be deployed.

PropTech-specific use of funds often includes:

- Product development (feature buildout, integrations with property management systems)

- Sales team expansion (enterprise sales in real estate requires experienced reps)

- Geographic expansion (real estate is local — new markets require local presence)

- Compliance and regulatory infrastructure

- Hardware/IoT deployment costs (if applicable)

Early-stage PropTech valuations typically fall in the 8-12x ARR range, though this varies significantly by category and growth rate. If you’re pre-revenue, comparable recent deals in your subcategory are more useful reference points than generic SaaS multiples.

The ESG Angle: Use It If It’s Real

ESG disclosure mandates are driving a wave of PropTech adoption. Buildings account for roughly 40% of global carbon emissions, and institutional real estate owners are under increasing pressure to measure, report, and reduce their environmental impact.

If your product helps with energy efficiency, carbon tracking, sustainability reporting, or green building certification, this isn’t a nice-to-have slide — it’s a core part of your value proposition. Institutional PropTech investors now explicitly screen for ESG impact. In 2024, dedicated ESG PropTech funds exceeded $1.1 billion.

But don’t greenwash. If your product’s ESG impact is marginal, don’t build your deck around it. Sophisticated real estate investors will see through surface-level sustainability claims immediately.

Common PropTech Pitch Deck Mistakes

Selling technology instead of outcomes. Real estate investors don’t care about your tech stack. They care about what it does to NOI, vacancy rates, maintenance costs, or transaction speed.

Ignoring regulatory complexity. Real estate is one of the most regulated industries in the world. If your pitch doesn’t address compliance — fair housing, AML, licensing, data privacy — you look naive to anyone who’s operated in the space.

Assuming SaaS benchmarks translate directly. PropTech SaaS has higher CAC, longer sales cycles, and different churn dynamics than horizontal SaaS. Use PropTech-specific benchmarks, or at minimum acknowledge the differences.

Underestimating the incumbent. The biggest competitor for most PropTech companies isn’t another startup — it’s the spreadsheet, the phone call, the “we’ve always done it this way” inertia. Your deck needs to show not just that your solution is better, but that you have a strategy to overcome adoption resistance.

One-size-fits-all decks. An institutional REIT investor evaluates opportunities completely differently than an angel who owns a few rental properties. At minimum, have two deck versions — one for institutional/VC investors, one for strategic real estate investors.

The Deck Is Your First Transaction

In real estate, everything is a transaction. Your pitch deck is the first one you’re conducting with your investor. It signals whether you understand the industry, respect the buyer’s intelligence, and can communicate value in terms that matter.

The PropTech founders who raise successfully don’t just build great products — they demonstrate that they understand how real estate capital evaluates, filters, and decides. That understanding starts on slide one and needs to hold through every page.

If your deck reads like a tech pitch that happens to mention buildings, go back to the drawing board. If you’re deciding whether to build it yourself or bring in outside help, it’s worth understanding how much a pitch deck costs and what you’re actually paying for at each level. If it reads like a real estate investment memo backed by exceptional technology, you’re in the right territory.

Need help building your PropTech pitch deck? This is exactly the kind of work I do — translating complex technology stories into the language that capital actually responds to. Get in touch.