Institutional capital evaluates asset and fund vehicles through an allocation lens, not a narrative one. This page explains how allocators, investment committees, and fiduciaries assess eligibility, diversification integrity, and portfolio fit within asset and fund capital structures. It applies the universal capital decision logic established in Hub 1, without redefining it. This is not execution guidance, not an asset allocation tutorial, and not a guide to building portfolios or raising capital. It documents how capital reviewers think, where they apply pressure, and why certain structures fail review—nothing more, nothing less.

Why Asset & Fund Capital Is Treated as an Allocation Problem

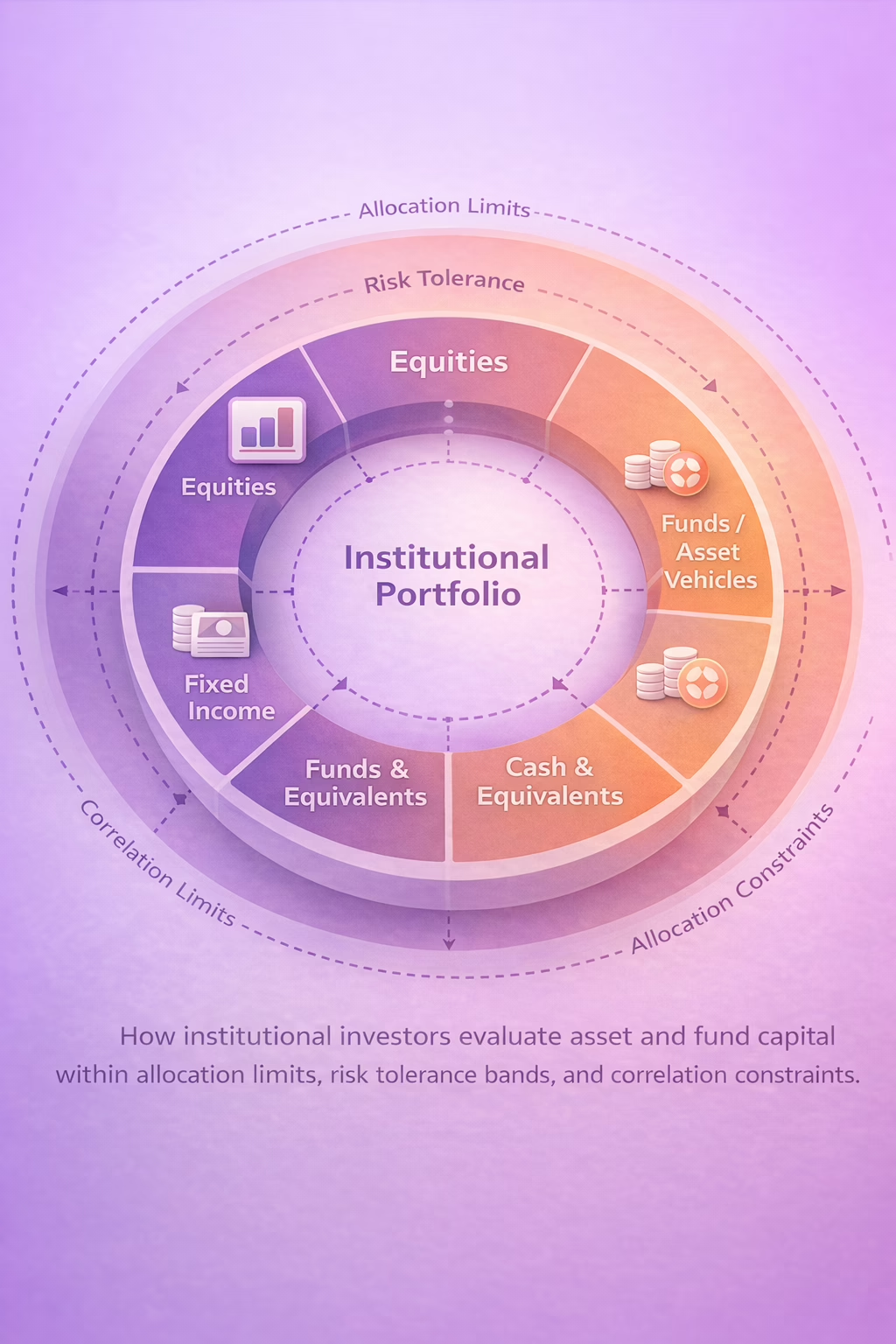

Asset and fund capital is constrained by its role inside larger investment portfolios. Unlike operating businesses, funds are not evaluated for growth narratives but for how they behave under allocation models, diversification requirements, and risk tolerance constraints.

Capital here is already scarce, already allocated, and already governed. The primary question is not whether an investment can generate returns, but whether it can occupy a defined asset class position without destabilizing the broader investment portfolio. Risk is non-linear because correlation, liquidity, and drawdown behavior matter more than upside scenarios.

For allocators, this sector is less about conviction and more about containment.

Allocation Integrity as the First Gate

The first evaluation filter is allocation coherence. Reviewers assess whether the asset allocation model presented is internally consistent and externally credible within an institutional portfolio.

Funds are examined for clarity of asset category, allocation strategy, and diversification claims. Ambiguity between stocks, bonds, cash equivalents, alternative assets, or hybrid structures immediately weakens eligibility. Allocation that appears opportunistic rather than deliberate signals governance risk.

Failures here typically stem from over-broad mandates, unclear allocation boundaries, or strategies that drift across asset classes without justification.

Diversification Claims and Correlation Risk

Diversification is treated as a measurable property, not a marketing concept. Committees evaluate whether diversification actually reduces portfolio risk or simply multiplies exposure across correlated assets.

Asset allocation funds claiming diversification are stress-tested against historical drawdowns, asset class correlations, and market index behavior. “Different assets” is not sufficient; what matters is whether those assets behave differently under stress.

Common rejection patterns include funds that diversify within a single risk factor, concentrate unknowingly in one asset class, or rely on diversification narratives unsupported by data.

Risk Tolerance and Downside Containment

Every asset allocation strategy is reviewed against explicit risk tolerance thresholds. Allocators evaluate how much downside the investment introduces relative to its expected contribution to the investment portfolio.

This includes volatility profiles, drawdown recovery timelines, liquidity constraints, and behavior across time horizons. Conservative asset allocation structures are scrutinized as closely as aggressive ones; misalignment between stated risk tolerance and actual exposure is treated as a governance failure.

Funds often fail this gate when their allocation implies a level of risk inconsistent with their stated investment goal or when downside scenarios are under-modeled.

Portfolio Fit Within Institutional Constraints

Institutional portfolios operate under constraints that retail investment strategies do not. These include rebalancing rules, capital reserve requirements, regulatory exposure, and long-term financial goals such as pension obligations or endowment preservation.

Evaluators assess whether the asset allocation can be integrated without disrupting existing allocation strategies. Even strong individual investments are rejected if they create rebalancing friction, liquidity mismatches, or disproportionate concentration at the portfolio level.

Failure commonly occurs when funds assume they will be evaluated in isolation rather than as one component among many investments.

Structural Failure Modes in Asset & Fund Evaluation

Rejections in this sector are rarely about performance forecasts. They arise from structural issues: unclear asset class definition, inconsistent allocation strategies, overstated diversification benefits, misaligned time horizons, or allocation models that cannot be maintained under real portfolio conditions.

Another frequent failure mode is reliance on familiar consumer investment language that does not map cleanly to institutional allocation logic. What many investors find intuitive, committees often find imprecise.

The Role of Artifacts in Asset & Fund Review

Pitch decks, models, and investment documents function as validation artifacts, not persuasion tools. They are used to confirm allocation discipline, portfolio assumptions, and compliance with investment mandates.

Artifacts can validate asset allocation models, diversification structure, and risk boundaries. They cannot compensate for misaligned asset categories, correct structural allocation flaws, or override portfolio-level constraints imposed by the allocator.

In this sector, documentation confirms fitness; it does not create it.

How Asset & Fund Capital Expresses Universal Capital Logic

Asset and fund evaluation is one expression of the broader institutional capital allocation framework. The same universal logic applies—eligibility, risk containment, governance, and portfolio alignment—but is executed through allocation models, diversification analysis, and asset class discipline rather than operating metrics.

Asset and fund capital expresses the same underlying capital eligibility and risk governance model, where allocation is permitted only after portfolio fit, downside containment, and mandate alignment are established at the institutional level.