Institutional capital allocation does not operate through persuasion, novelty, or narrative strength.

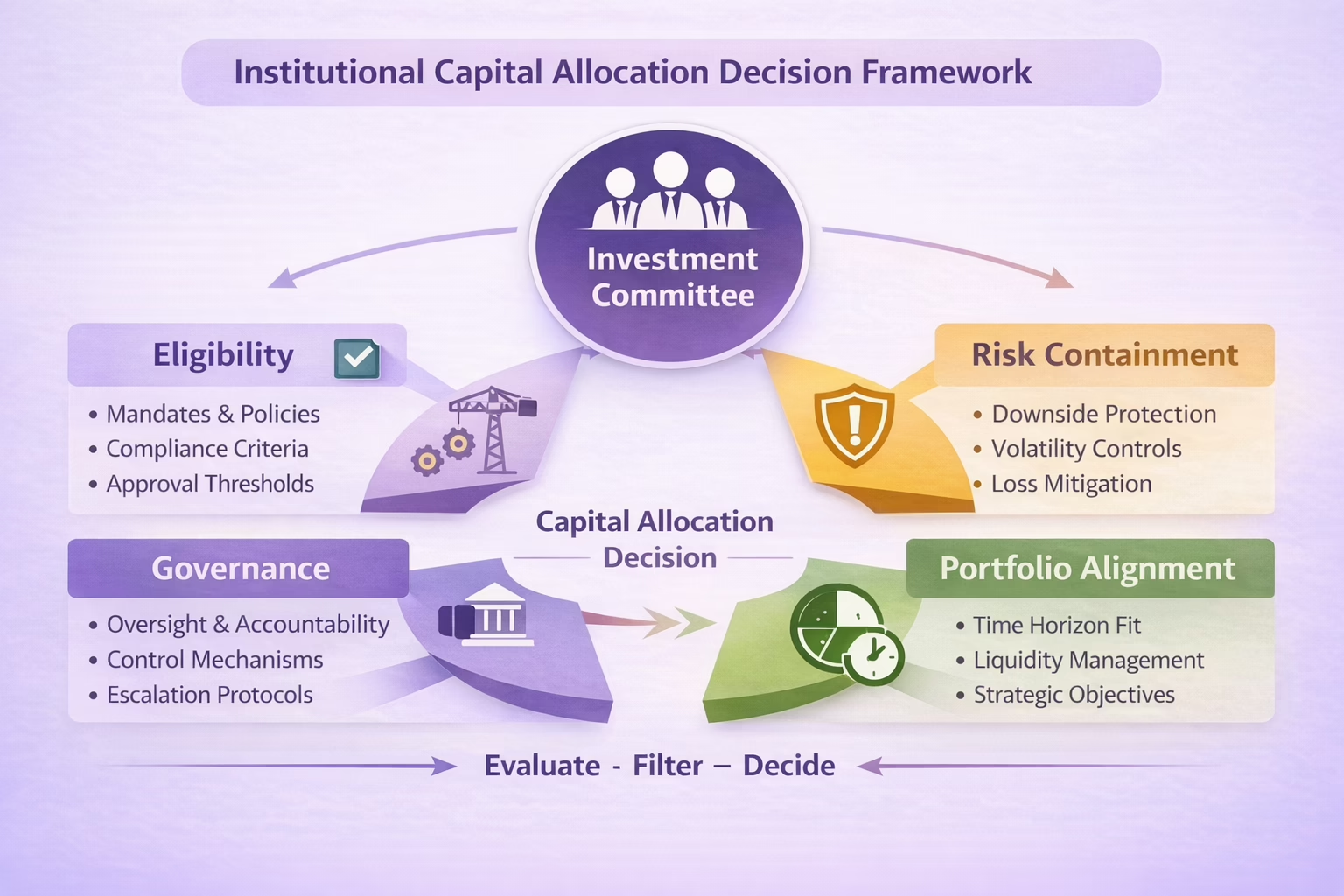

Institutional investors allocate capital according to mandate, eligibility, risk containment, governance, and alignment across time horizons.

This page defines the universal decision logic investment committees, asset managers, and capital allocators use to determine whether an investment, asset allocation, or portfolio exposure is permitted—independent of sector, asset class, or market cycle.

It does not explain how to pitch, structure proposals, or execute strategies; it documents how institutional capital evaluates allocation decisions before any capital is committed.

What Institutional Capital Decision-Making Actually Is

Institutional capital decision-making is the governed process by which institutional investors, investment managers, and allocation committees determine whether capital allocation to an asset, investment opportunity, or portfolio position satisfies predefined eligibility, risk, governance, and alignment constraints before considering potential return. Capital is stewarded on behalf of beneficiaries, plan sponsors, shareholders, or stakeholders, under fiduciary duty and formal investment policy.

Allocation decisions are evaluated against mandate, liquidity requirements, risk tolerance, and portfolio construction limits designed to preserve capital and trust across market cycles. Attractiveness is assessed only after eligibility is established; upside is considered only after downside containment; and investment opportunities are reviewed only within approved governance and incentive structures. Artifacts such as pitch decks, financial models, and investment memos function as inputs for verification and documentation—not persuasion—and cannot override allocation policy, investment objectives, or capital preservation rules.

Eligibility Before Attractiveness

Institutional capital first determines whether a proposed investment or asset allocation is permitted under mandate, investment policy, and portfolio constraints. Committees assess whether the opportunity fits the defined investable universe, complies with governing rules, and aligns with stated investment objectives.

This filter exists to enforce fiduciary duty and prevent discretionary drift across asset classes, markets, or managers. Proposals that fall outside mandate scope, conflict with policy, or lack required approvals fail at this stage regardless of projected returns, diversification benefits, or strategic narrative.

Capital Preservation Before Upside

Institutional investors prioritize protection of principal before pursuit of return. Committees evaluate possible loss of principal, downside exposure, volatility, and impairment risk before considering upside potential or allocation size.

This filter exists to safeguard total assets and maintain trust with beneficiaries and stakeholders. Investments with unbounded loss profiles, opaque downside scenarios, or correlated exposure across the investment portfolio fail here, even when expected returns appear compelling.

Risk Containment Before Growth

Growth is acceptable only when risk can be segmented, monitored, and controlled at the portfolio level. Committees assess whether exposure expands faster than oversight, controls, or governance mechanisms.

This filter exists to prevent uncontrolled scaling of failure across asset classes or private markets. Investment opportunities dependent on single points of failure, non-auditable controls, or concentrated operational risk fail regardless of growth projections or market opportunity.

Governance Before Opportunity

Institutional capital evaluates governance structures before evaluating opportunity size. Committees require clear authority, oversight, escalation rights, enforcement mechanisms, and accountability across management teams and counterparties.

This filter exists because governance converts claims into enforceable obligations. Proposals with concentrated discretion, weak oversight, unclear decision rights, or unenforceable protections fail regardless of portfolio fit or return expectations.

Incentive Compatibility

Committees analyze whether incentives predict behavior consistent with capital preservation, mandate compliance, and long-term portfolio objectives. Incentive structures are evaluated across investment managers, general partners, and counterparties.

This filter exists to reduce agency risk. Allocation structures that reward volume over quality, upside without downside participation, or speed over control fail this test, regardless of headline performance or past results.

Time-Horizon Alignment

Capital allocation must align with the institutional investor’s time horizon for liquidity, reporting, and risk management. Committees evaluate whether investment horizons, cash-flow timing, and liquidity terms match portfolio needs and beneficiary obligations.

This filter exists to avoid forced exits, liquidity stress, and value destruction. Investments with illiquid structures, mismatched reporting cycles, or unrealistic liquidity assumptions fail even when long-term returns appear attractive.

Decision Reversibility

Institutional capital assesses whether allocation decisions preserve optionality. Committees examine the ability to pause, exit, restructure, or remediate exposure under adverse conditions.

This filter exists to limit the cost of error in uncertain environments. Irreversible commitments without commensurate control, compensation, or governance protections fail regardless of strategic rationale.

Why Most Proposals Fail

Most proposals are rejected for structural reasons, not presentation quality. Failures occur when eligibility is breached, capital preservation cannot be demonstrated, risk is uncontained, governance is unenforceable, incentives are misaligned, liquidity conflicts with portfolio needs, or decisions eliminate reversibility.

Institutional investors do not optimize for narrative appeal or urgency. Allocation decisions are binary at each gate because mandates, fiduciary duties, and investment policy constraints are not negotiable.

The Role of Artifacts in Institutional Capital Decisions

Artifacts such as pitch decks, financial models, investment memoranda, and presentations serve as inputs for documentation, verification, and investment decision records. They support consistency checks, scenario analysis, and portfolio impact assessment.

Artifacts cannot expand mandate, alter allocation strategy, waive policy, substitute for governance, or convert ineligible risk into eligible capital allocation.

Common Misalignments Between Proposers and Allocators

Proposers often assume capital allocation decisions are comparative, iterative, or persuadable. Institutional allocators operate through eligibility gates, risk filters, and mandate constraints.

This misalignment leads to proposals optimized for attractiveness rather than investability, urgency rather than risk containment, and narrative rather than enforceable structure—resulting in rejection regardless of opportunity size.

How This Logic Manifests Across Institutional Environments

The decision logic described above is universal across institutional capital. What differs across environments—pension funds, endowments, sovereign allocators, asset managers, or private markets—are thresholds, documentation standards, and enforcement mechanisms defined by mandate and regulation.

The order of evaluation does not change. Only the measurement context, reporting requirements, and portfolio constraints differ.